TODAY’S STUDY: HOW WIND AND NAT GAS CAN MAKE EACH OTHER BETTER

Variance Analysis of Wind and Natural Gas Generation under Different Market Structures: Some Observations

Brian Bush, Thomas Jenkin, David Lipowicz, and Douglas J. Arent, January 2012 (National Renewable Energy Laboratory)

Executive Summary

An important area of current research is whether large-scale penetration of variable renewable generation such as wind and solar power pose economic and operational burdens on the electricity system. In such scenarios, this issue has also raised considerable interest in the potential role and value of electricity storage as a method of mitigating variability in generation associated with the inherently variable nature of these forms of generation. At the same time, a number of studies have pointed to the potential benefits of renewable generation as a hedge against the volatility and potential escalation of fossil fuel prices. Prior research and this work suggest that the lack of correlation of renewable energy costs with fossil fuel prices means that adding large amounts of wind or solar generation may also reduce the volatility of system-wide electricity costs. Such variance reduction in overall system costs may be of significant value to consumers due to risk aversion. In contrast to this observation, other studies have focused on returns in restructured markets and noted that, in deregulated markets, baseload natural gas power generation may be relatively more attractive to investors because—unlike wind generation—peak power prices are often strongly correlated to natural gas prices.

click to enlarge

click to enlargeThe analysis in this report recognizes that the potential value of risk mitigation associated with wind generation and natural gas generation may depend on whether one considers the consumer’s perspective or the investor’s perspective and whether the market is regulated or deregulated. We analyze the risk and return trade-offs for wind and natural gas generation for deregulated markets based on hourly prices and load over a 10-year period using historical data in the PJM Interconnection (PJM) from 1999 to 2008. Similar analysis is then simulated and evaluated for regulated markets under certain assumptions. Estimating the absolute value, as opposed to the relative value, of variance reduction will also depend on assumptions about risk aversion and other consumer preferences, such as loss aversion, and this is discussed. Some key observations include:

click to enlarge

click to enlargeIn a deregulated market such as PJM,

• Returns for natural gas generation are partially hedged because power prices are often set by natural gas generation, though with significant seasonal variations.

• Returns for wind generation are better hedged than natural gas generation because wind often operates in off-peak hours, where power prices are much less volatile and less correlated with natural gas prices, whereas natural gas generation operation is focused more heavily during peak hours.3

• The impact of incremental net revenue from tax credits, such as production tax credits (PTCs) or other sources of revenue, can have a significant impact on the risk return relationship. In PJM over this period with credits, wind was found to be dominant in terms of risk and reward; that is, it had both greatest returns and the lowest risk, as measured by standard deviation of returns.

• More generally, without PTCs investors may benefit from investing in both wind and natural gas generation, with the optimal mixture depending on the investor’s risk aversion (and perhaps also loss aversion) preferences due to well-known lack of correlation effects.

click to enlarge

click to enlarge• While the opportunity for investors to diversify in broader markets may reduce some of the variance reduction benefits of investing in different electric technologies, it is unlikely to completely eliminate these benefits in the electric sector where power prices are often very volatile and positively skewed, which has implications for financial distress.

• Consumers, especially smaller commercial and residential consumers, may benefit from reductions in the variance of electricity prices due to risk aversion and loss aversion effects.

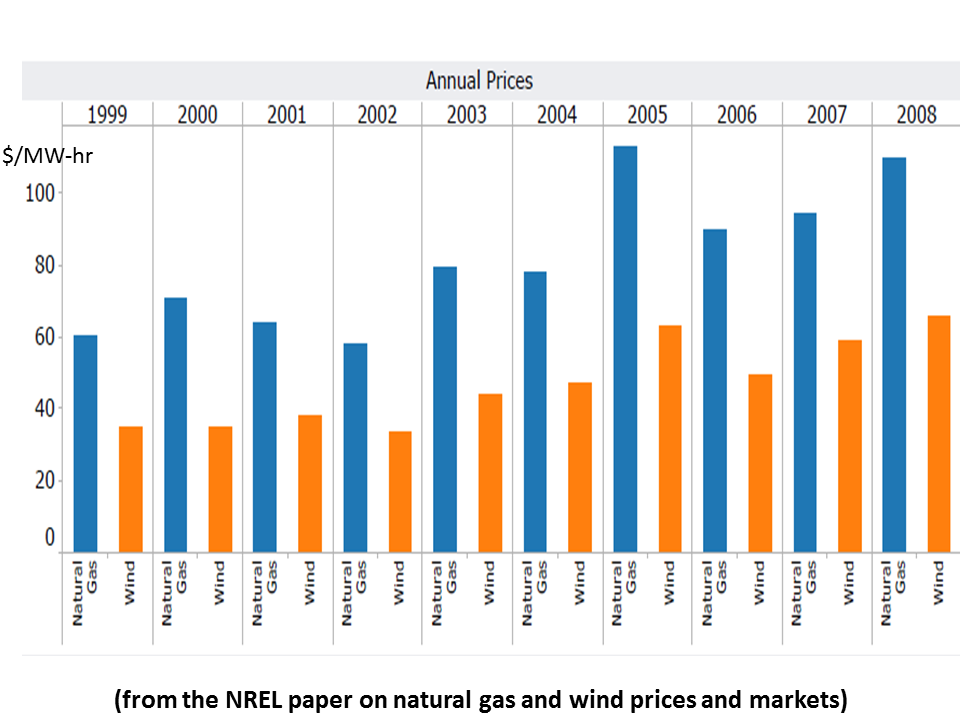

• The levelized cost of energy (LCOE) of different technologies is not directly comparable if they operate in different hours because the value of electricity differs significantly throughout each day. This variation reflects the daily load profile, with hourly load and hourly power prices also showing strong seasonal effects. This effect can be seen in our analysis of PJM data when comparing the difference in the average annualized hourly price of variable wind generation and dispatchable natural gas generation.

click to enlarge

click to enlargeIn a regulated market:

• The inherent nature of regulated markets means that producers earn, with some caveats, a utility-designated rate of return. A consequence of this is that the risk associated with fuel costs is passed on to the consumer. The “cost-plus” nature of regulation means that consumers also bear some increased risk associated with poor investment decisions. Consumers are partly compensated for this because the producer may be willing to accept a lower expected rate of return compared to deregulated markets.

• For consumers, who are generally risk averse, the reduced variation in electricity prices (and hence consumer costs) because of wind’s lack of correlation with other system costs should have value (as has been suggested by others). Loss aversion also may place a value on variance reduction of electricity prices and consumer costs.

• Simplified mean variance cost optimization techniques using annualized LCOEs for the power sector often fail because the assets within the portfolio are too dissimilar (e.g., baseload versus peaking or either of these versus a variable or non-dispatchable resources such as wind or solar).

click to enlarge

click to enlarge• A variance reduction-based technique could, however, be used more broadly under more sophisticated representation of system costs where the hourly operation of the technologies is modeled more explicitly. Specifically for a regulated electric system, the concept of lowest-cost planning could be refined to have an array of “least-cost planning” solutions corresponding to different variances, where the values of the expected annualized system cost and the standard deviation of the annualized system cost are physical properties of the electric system that are completely independent of any risk or loss aversion preferences. The value of variance reduction could then reflect both risk aversion and loss aversion. We discuss explicitly how to estimate the difference in the economic utility between alternative system-based, expected costcost variance choices, including the impact of the distribution being positively skewed toward higher costs.

In conclusion, we should point out that while some of the observations and findings may be generally applicable, others are empirical observations for a specific location and a specific time period under specific technology cost and performance assumptions.

posted by Herman K. Trabish @ 5:29 AM

![]()

0 Comments:

Post a Comment

<< Home