OFFSHORE WIND, THE WAY FORWARD

Report states how to build a UK offshore wind powerhouse

29 June 2010 (RenewableUK)

THE POINT

The courage shown by the new UK coalition government in looking hard economic times square in the eye and taking on the austerity measures needed is winning praise around the world and across the political spectrum.

For the energy sector, this comes as no surprise. The British have long demonstrated these paired traits of realism and the determination to act. They met the opportunity of North Sea oil with traditional British sea-going dynamism. As those oil supplies began to peak, they began making nuclear plans. As the danger and unaffordability of nuclear power became undeniable, courageous British leaders once again chose to go down to the sea, to develop the UK's immense offshore wind and ocean wave and tidal energies.

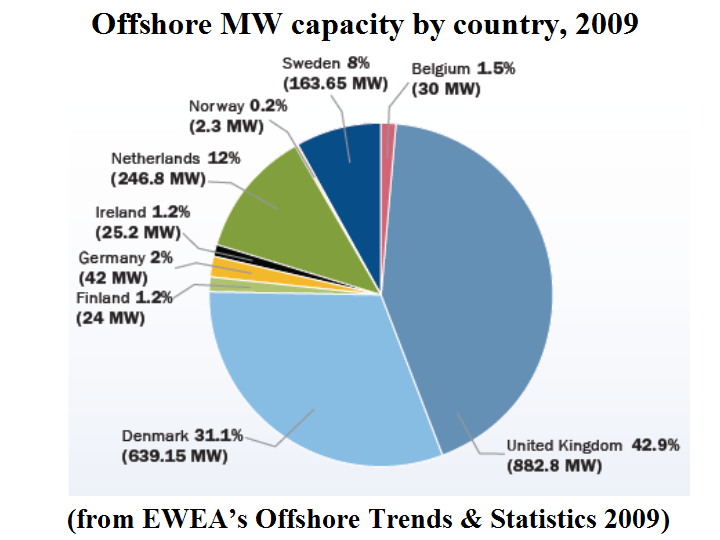

In response to initial commitments from the UK government to fund British offshore wind infrastructure expansion, some of the biggest turbine manufacturers in the world (Siemens, Clipper, Mitsubishi, GE) have commited to a presence. At the end of 2009, the UK had almost 900 megawatts of installed offshore capacity.

UK Offshore Wind: Building an Industry; Analysis and scenarios for industrial development is a detailed report on what Britain needs to unhesitatingly but methodically advance its offshore industries and bring more major private sector investment into the country. It provides specifics on siting factories and preparing ports, how much that will cost and what the economic benefits will be from the investment.

click to enlarge

click to enlargeThe core insight offered in the study is that an industry's way forward can be successful or fail according to the infrastructure planning and preparation that preceeds expansion.

The study calls on the coalition government to commit the 60 million pounds set aside to prepare port infrastructure and take the lead in building new manufacturing capacity to prepare the nation not only to build its own New Energy capacity but to take a dominant role in the EU market as well. The report concludes that methodical, effective investment will lead to a stable offshore wind industry that will create 45,000 new British manufacturing jobs. It predicts that either (a) allowing offshore wind to grow too fast or (b) failing to plan and invest will result in the same “missed opportunity.”

Meanwhile, the Obama administration – which took office promising to facilitate the development of U.S. ocean energy assets – is now bogged down in the complexities created by BP’s misrepresentations and the clamor for stronger offshore regulatory protections. The best it has managed in streamlining the 7-to-10 year siting and permitting challenges to ocean energy development are announcements of memoranda of understanding (MOUs) between the Department of the Interior (DOI) and the Department of Energy (DOE) and between DOI, DOE and the Army Corps of Engineers.

In other words, while the UK is working out the details of turning its ocean energy potential into industrial power, the U.S. is working on getting government agencies to communicate more effectively.

Talk about a missed opportunity…

click to enlarge

click to enlargeTHE DETAILS

The report describes 2 scenarios for UK offshore wind development from 2015 to 2030. Scenarios detail assumptions about hardware manufacture and installation..

(1) The Aggregated Developer Appetite scenario: sees capacity ramping up so fast it virtually prevents growth in the longer run by overburdening an underdeveloped supply chain and inadequate infrastructure.

(2) The Healthy Industry scenario: creates a “substantial and sustainable” manufacturing base and at least 45,000 UK jobs. Requires action in the next 12-24 months on new factory sites.

(3) The Low Added Value scenario: achieves the UK government's Renewable Energy Strategy, but without building UK manufacturing and provides for ocean energy production but misses the opportunity for UK jobs and industrial growth.

The Siemens, Clipper, Mitsubishi and GE plans – the result of the UK government’s offshore wind development goals and policies – are expected to initiate a major supply chain expansion.

Further government investment in port and factory infrastructure will demonstrate long-term market potential that will expand the domestic industry into an industrial powerhouse.

click to enlarge

click to enlargeThe Crown Estate manages offshore wind development in the UK and has organized projects into a series of “Rounds” (2, 2.5, 3 and Scottish Territorial Waters, STW) extending to 2030.

Aggregated Developer Appetite:

(1) per year of new capacity

(2) cumulative capacity by 2015, 42.7GW by 2020

(3) stress on the UK transmission system

(4) installations peak in 2018 at almost 8GW before declining sharply over

the next three years.

(5) will require an early Round 4 to prevent a sharp drop off in development

(6) will build a strong domestic market if the government makes quick investment decisions on new domestic manufacturing plants

A Healthy Industry:

(1) less sudden, longer-term, more stable growth with a slowing after 2022

(2) strong and sustainable deployment, matched with transmission expansion and good supply chain development brings in major industry players and leads to UK economic benefits

(3) 3.3 GW of new capacity per year

(4) requires 5 new turbine plants by 2014

(5) 7.7 GW cumulative capacity installed in 2015, 23.2GW by 2020

Low Added Value:

(1) slow growth, project delays, less supply chain development, fewer new manufacturers: A missed opportunity

(2) 2 GW per year new capacity

(3) does not drive transmission expansion

(4) 6.6 GW cumulative capacity installed in 2015, 14.1 GW by 2020.

click to enlarge

click to enlargeExpansion will require better UK transmission and an integrated European Grid. Sustained expansion will require UK manufacturers to sell to the wider EU market.

~10,000 turbines and foundations will be required between 2015 and 2030. 12,000+ km of array cabling will be needed, 8,500+ km of export cable.

2016 is expected to be the hinge year in which manufacturing capacity meets growth demand or the industry dwindles and the opportunity is missed. The UK will need 22 factories for turbines, foundations and cables. To have this capacity, investment must be committed now. The cumulative cost is estimated at £1 billion+.

For the unsustainable Aggregated Developer Appetite scenario, 8 new turbine manufacturing facilities will be needed by 2015 at an estimated cost of £720 million.

Beyond peak UK offshore growth (in ~2022), the manufacturing capacity must be used to serve EU offshore development. Comparing growth scenarios for the UK with predicted growth of the EU offshore market suggests the EU market will emerge at the ideal time.

Rapid EU offshore expansion is expected after 2019. EU installations exceed UK installations after 2022. By 2024, the cumulative installed capacity of the rest of the EU will exceed that of the UK.

click to enlarge

click to enlargeShould the UK government invest only enough to achieve the Low Added Value scenario, it will be unprepared to seize the opportunity of being a supplier for the EU expansion. The German industry is expected to be highly competitive.

North Sea oil & gas reserves may be peaking but they are still in production. UK offshore expansion will produce competition for (1) Heavy Lift Vessels and (2) Engineering Services. As oil & gas reserves fall off, competition will continue because the oil & gas industry will require the vessels and the services for decommissioning.

An estimated 1.6 million tonnes of oil & gas facilities will be decommissioned between 2010 and 2025, requiring an estimated 8,900 vessel-days.

The good news: The UK oil & gas industry has 40+ years of experience working in the North Sea and can teach offshore wind industry installers and designers a great deal about preventing cost overruns and delays, and about making equipment to match the rugged environment.

To seize the opportunity: (1) A £60 million investment in ports that will attract the needed £1 billion of private investment starting in 2011, and (2) further government investment in planning, skills and training, research, design and demonstration.

click to enlarge

click to enlargeActions required from the new government:

(1) Reaffirm support for offshore wind

(2) Quickly clarify support mechanisms

(3) Decide on post-2014 policies and investments by 2011

(4) Implement changes to the new Feed-in Tariff (FiT)

(5) Get agreement between government and industry on targets

(6) Clarify post-2020 plans

Actions required from the new government on resources:

(1) Guarantee funding from government

(2) Designation of development and no-go zones

Actions required to sustain financing:

(1) Strong and stable policy of support

(2) A ‘green bank’ to accelerate and leverage private sector investment and guide government policy

Actions required to build needed transmission:

(1) Allow developers to build their own interconnects

(2) Assess projects individually to avoid stranded assets

(3) Provide strong incentives for onshore Transmission Owners (National Grid, Scottish Power, and Scottish and Southern Energy) to expand and upgrade

(5) Review transmission charges

click to enlarge

click to enlargeActions required for port development:

(1) Accelerate the selection of 3 or 4 ports that will become offshore wind manufacturing hubs

(2) Fund the selected ports with the pledged £60 million now

(3) Provide incentives to grow a supply chain around the key ports

Actions required to grow a supply chain:

(1) A central planning body

(2) Assistance to locate suppliers near turbine manufacturers and assemblers

(3) Fund support manufacturing

(4) Tax breaks for supply chain players

Actions required to build a skilled workforce:

(1) A national skills strategy that prioritizes the skills needed

(2) Collaboration between government, industry and educators to deliver the skills and education needed

(3) Funding

(4) Centers of excellence to provide special skills

(5) Support to transfer workers to where they are needed and give them the training they need

Actions required for RD&D:

(1) A national wind energy RD&D program

(2) Testing and demonstration facilities

(3) Fast-tracking of test sites

(4) Funding of the construction of offshore wind demonstration projects

(5) Promote Joint Industry Projects

click to enlarge

click to enlargeQUOTES

- Maria McCaffery MBE and CEO, BWEA: "Offshore wind presents the UK with a major opportunity to not only reconfigure its energy production towards clean and renewable sources, but a once-in-generation opportunity to build a home-grown manufacturing and R&D base for a new industry, and become the world leader in the field…Without firmer Government strategy we will get an offshore wind industry which produces clean energy for the UK, but one for the which the production facilities, and the manufacturing jobs are located elsewhere. If ambitious targets are agreed, and the Government acts now…wind can be the sector which drives forward the Coalition's pledge to rebalance the economy and create jobs."

click to enlarge

click to enlarge- From the report: "The Aggregated Developer Appetite scenario sees rapid deployment of offshore wind capacity and necessitates very high investment into the supply chain. This scenario is seen as possible by industry but would require major commitment from government…The supply chain would need to begin building now and without delay…The other prerequisite would be the further growth of the UK domestic and European export market to sustain the supply chain…The challenges of consenting, financing, contracting and building the UK’s large project portfolio are considerable…"

click to enlarge

click to enlarge- From the report: "The Healthy Industry scenario shows long-term sustainable demand in the market…At least five turbine plants will be required for the capacity expected in the UK, which will allow healthy competition between manufacturers…[This level of competition will help drive technology progression and should result in cost reduction…"

click to enlarge

click to enlarge- From the report: "The Low Added Value scenario shows the effects of an average two year delay to many projects together with a scaling back in project size. Although the slower delivery curve will ease the scaling up of capacity that is required…the much lower rate of delivery makes it more difficult for the UK to support multiple turbine manufacturers and will limit the extent to which the UK supply chain can develop…"

posted by Herman K. Trabish @ 5:59 AM

![]()

0 Comments:

Post a Comment

<< Home