TODAY’S STUDY: THE RISKIEST ENERGY IN THE WORLD

Oil & Gas Majors: Fact Sheets

August 2014 (Carbon Tracker Initiative)

Executive Summary

Overview: Key Points

1. The oil & gas sector is currently facing pressure from investors to focus on capital discipline, and several majors have stated that their capex will either fall or stay flat over the coming years.

2. In order to sustain shareholder returns, companies should focus on low cost projects, deferring or cancelling projects with high breakeven costs. Capital could be redeployed to share buybacks or increased dividends.

3. This process has already started, particularly in the Canadian oil sands sector. The majors’ portfolios include several significant arctic and deep water/ultra-deep water projects which could prove low return assets in a low-demand scenario. Deferral or cancellation of these might protect shareholder returns.

4. Collectively, the majors have a potential capital spend of $548bn over the period 2014-2025 on projects that require a market price of at least $95/bbl for sanction (34% of total capex on all their projects).

5. $357bn of this is on high cost projects that are yet to be developed. Such projects are candidates for deferral or cancellation.

6. Investors may wish to push companies for more detailed disclosure of project level economics, and challenge developments that carry an undue risk of wasting capital and destroying value.

click to enlarge

click to enlargeIntroduction

CTI has demonstrated in its research the mismatch between continuing growth in oil demand and reducing carbon emissions to limit global warming. Our most recent research with ETA to produce the carbon cost supply curve for oil indicates that there is significant potential production that could be considered both high cost and in excess of a carbon budget. We have focused our research on undeveloped projects that, allowing for a $15/bbl contingency, would need a $95/bbl market price or above to be sanctioned (i.e. a market price required for sanction of $95/bbl is equivalent to a project breakeven price of $80/bbl), as they are the marginal barrels that could be exposed to a lower demand and price scenario in the future.

This note examines the seven largest publicly listed oil companies’ potential future project portfolios looking at production and capex using Rystad Energy’s UCube Upstream database (as at July 2014). “Capex” and “production” in this note (amongst other terms) are thus based on Rystad’s analysis and expectations of the company’s potential projects. The companies’ planned or realised capex and production may differ from these projections. Where possible we have sought to verify the status of the projects at the time of writing. A $15/bbl premium has been included in the required market prices for sanction of oil sands projects to account for additional transport costs. Individual company portfolios and exposure to high-risk projects are contained in the individual company factsheets which accompany this summary comparison.

click to enlarge

click to enlargeProjects Shelved

There have been some recent examples of projects being put on ice by the majors. In the oil sands in 2014, Total and Suncor have shelved the $11bn Joslyn project1 and Shell put on hold its Pierre River project2 . Deepwater projects have also been deferred with BP not proceeding with its Mad Dog extension in the Gulf of Mexico3 , and Chevron reviewing its $10bn Rosebank project in the North Sea4. In the Arctic, Statoil and Eni have deferred a decision on the $15.5bn Johan Castberg project5.

Some companies are therefore already starting to demonstrate greater capital discipline amidst falling group returns. This is becoming increasingly necessary as near term cash flows are not sufficient to maintain both dividends and capital expenditure plans. In the short-term companies have squared the circle by selling assets or adding debt. Cutting capital spend should improve corporate cash flow statements as could new cash flow from new projects. But with some companies continuing to sanction projects at the high end of the cost curve, hence increasing operational gearing, shareholder value could be put at risk should demand and hence oil prices be lower than the majors anticipate.

click to enlarge

click to enlargePotential Production

• Shell has one of the highest proportions of high-cost potential production, with 45% requiring a market price of $75/bbl and 30% requiring at least $95/bbl, although ConocoPhillips has the highest cost production profile with 56% and 36% respectively.

• Eni and BP have the portfolios with the lowest oil market price requirements, 30% and 40% of which respectively requiring above $75/bbl and 15% and 21% of which respectively requiring at least $95/bbl.

click to enlarge

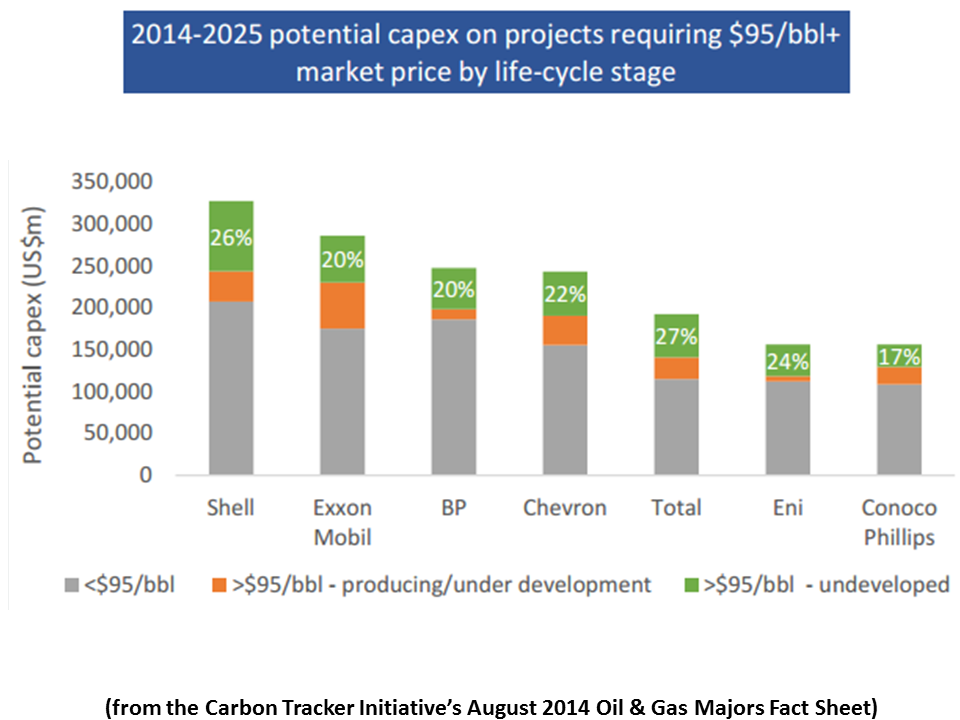

click to enlargePotential Capex

• Turning to capital spend in the nearer term (2014-2025) Total and ExxonMobil’s capital budgets have some of the highest oil price requirements, with 60% and 68% respectively on potential projects requiring a market price of at least $75/bbl for sanction and 40% and 39% requiring at least $95/bbl (including a $15/bbl contingency allowance).

• Shell is not dissimilar with 65% of its potential capex requiring a market price over $75/bbl and 37% over $95/bbl.

• BP and Eni again have the lowest proportion of high-price requirements, with 25% and 28% on projects that need a market price of at least $95/bbl for sanction, although Eni and ConocoPhillips have the least exposure to projects that would be need at least $75/bbl with 54% and 59%.

• Looking at just undeveloped projects, 27% of Total’s and 26% of Shell’s capex in this category requires a market price of $95/bbl+.

• By contrast, only 17% of ConocoPhillips’s potential capex budget is on high-cost projects that are as yet undeveloped. BP and Exxon have the second lowest exposure with with 20% of their capex in this category.

click to enlarge

click to enlarge• “Undeveloped” in this sense comprises fields where a discovery has been made (“discovery”) and where no discovery has been made (“undiscovered”)

• Oil sands projects account for 27% and 26% of Shell and ConocoPhillips’s high-cost potential development spend.

• Capital spend on undeveloped, high-break even projects is heavily biased towards the unconventional category, with just 14% of overall potential spend on conventional projects.

• BP and Total have particularly high exposure to deep water developments, with deep water and ultra-deep water in aggregate representing 78% and 73% of potential high cost spend respectively.

• ConocoPhillips is heavily biased towards arctic projects proportionately, which represent 24% of potential spend compared to an average of 5% amongst the other majors.

click to enlarge

click to enlargeCancellation Candidates

Focusing on individual projects for each company, there are a number of undeveloped, high-cost projects which are prime candidates for cancellation…The top twenty largest projects which represent high-risk, high-cost options for the oil majors…are primarily a mix of Alberta oil sands and deep water projects in the Atlantic, which would represent $91 billion of capital (over the period 2014-25). This capital could instead be returned to shareholders rather than being put at risk in projects that are already high cost and low return. Such projects have high operational gearing, putting shareholder returns at risk in a low oil price environment.

Key Questions

As well as specific questions on high cost projects and risk concentration identified for each company, investors should continue to push for disclosure on the following issues across the sector:

1. How does continuing dependence on oil fit with the imperative to tackle climate change recognised by most oil companies?

2. How would a range of oil prices impact your project economics and hence future earnings?

3. How does the current strategy of reinvesting revenues in high cost oil projects deliver shareholder value in a low demand, low price scenario?

posted by Herman K. Trabish @ 7:02 AM

![]()

0 Comments:

Post a Comment

<< Home