TODAY’S STUDY: WORLD WIND COMES ON

2014 Half-Year Report

September 2014 (World Wind Energy Association)

Worldwide Wind Market recovered: Wind Capacity over 336 Gigawatts

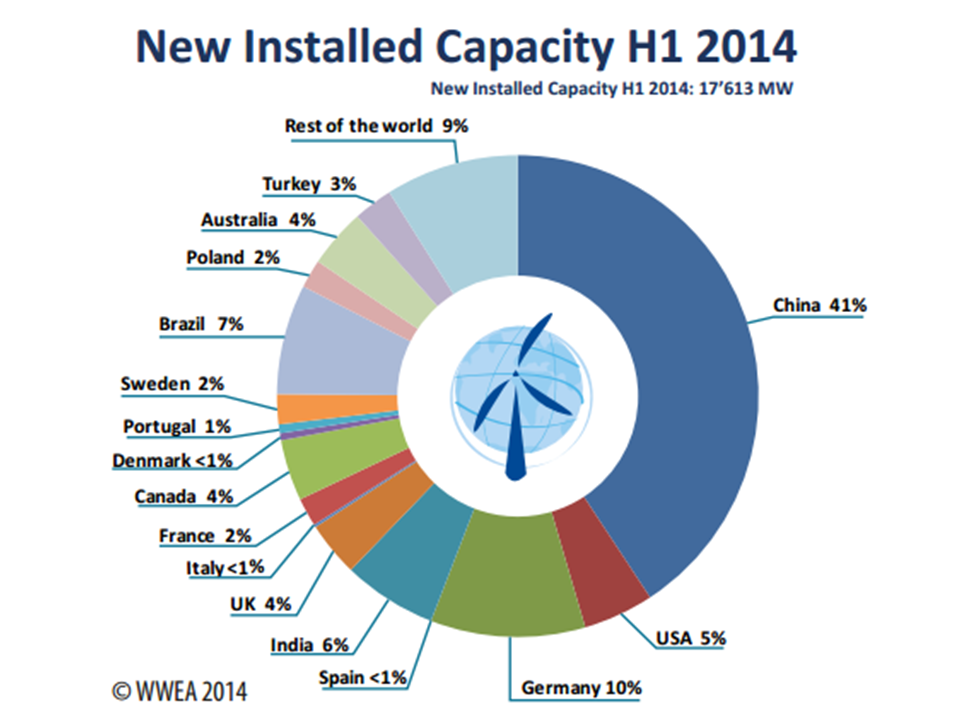

- 17,6 GW of new installations in the ¬rst half of 2014, after 14 GW in 2013

- Worldwide wind capacity has reached 336 GW, 360 GW expected for full year

- Asia overtakes Europe as leading wind continent

- China close to 100 GW of installed capacity

- Newcomer Brazil: third largest market for new wind turbines

- 360 GW expected by end of 2014

The worldwide wind capacity reached 336’327 MW by the end of June 2014, out of which 17’613 MW were added in the ¬rst six months of 2014. This increase is a substantially higher than in the ¬rst half of 2013 and 2012, when 13,9 GW and 16,4 GW were added respectively. The total worldwide installed wind capacity by mid-2014 will generate around 4 % of the world’s electricity demand. The global wind capacity grew by 5,5% within six months (after 5 % in the same period in 2013 and 7,3 % in 2012) and by 13,5 % on an annual basis (mid-2014 compared with mid-2013). In comparison, the annual growth rate in 2013 was lower at 12,8 %.

Reasons for the relatively positive development of the worldwide wind markets certainly include the economic advantages of wind power and its increasing competitiveness relative to other sources of electricity, as well as the pressing need to implement emission free technologies in order to mitigate climate change and air pollution.

c

cTop Wind Markets 2014: China, Germany, Brazil, India, and USA

The ¬ve traditional wind countries- China, USA, Germany, Spain and India- still collectively represent a 72 % share of the global wind capacity. In terms of newly added capacity, the share of the Big Five has increased from 57 % to 62%. The Chinese market showed a very strong performance and added 7,1 GW, substantially more than in the preceding years. China reached a total wind capacity of 98 GW in June 2014 and has undoubtedly by now crossed the 100 GW mark.

Germany performed strongly as well, adding 1,8 GW within the ¬rst half year. This new record no doubt comes partly in anticipation of changes in the renewable energy legislation, which may lead to a slow-down of the German market in the coming years.

For the ¬rst time, Brazil has entered the top group by becoming the third largest market for new wind turbines, with 1,3 GW of new capacity representing 7 % of all new wind turbine sales. With this, Brazil has been able to extend its undisputed leadership in Latin America.

India kept clearly its position as Asian number two and worldwide number ¬ve, with 1,1 GW of new wind capacity.

The US market, after its e ective collapse in 2013, has shown strong signs of recovery, with a market size of 835 MW, slightly ahead of Canada (723 MW), Australia (699 MW) and the United Kingdom which halved its market size and installed 649 MW in the ¬rst half of 2014.

The Spanish market, however, has not contributed to the overall growth in 2014, as it has come to a virtual standstill, with only 0,1 MW of new installations in the ¬rst half of 2014.

As was the case in 2013, four countries installed more than 1 GW each in the ¬rst half of 2014: China (7,1 GW of new capacity), Germany (1,8 GW), Brazil (1,3 GW) and India (1,1 GW).

The top ten wind countries show a similar picture in the ¬rst half of 2014, although on a slightly higher performance basis. Five countries performed stronger than in 2013: China, USA, Germany, France and Canada. Five countries saw a decreasing market: Spain, UK, Italy, Denmark and, to a lesser degree, India. Spain and Italy saw practically a total standstill, with only 0,1 MW and 30 MW respectively of new capacity installed. Poland is now in the list of top 15 countries by installed capacity while Japan dropped out.

target="_blank"

target="_blank"Dynamic Markets to be found on all Continents

It is important to note that for the ¬rst time, the most dynamic markets are found on all continents: the ten largest markets for new wind turbines included next to China, India and Germany, included Brazil (1’301 MW), USA (835 MW), Canada (723 MW), Australia (699 MW), UK (649 MW), Sweden (354 MW) and Poland (337 MW). New wind farms have also been installed in South Africa and further African countries, so that this continent has obviously entered the race to catch up with the rest of the world.

target="_blank"

target="_blank"Asia: The new leader on total installed capacity

With 36,9 % of the global installed capacity, Asia is now the continent with the most wind energy installated, suspassing Europe, which accounts for 36,7 %.

Again in 2014, China has been by far the largest single wind market, adding 7,1 GW in six months; this is signi¬cantly more than the same period of the previous year, when 5,5 GW were erected. China accounted for 41 % of the world market for new wind turbines. By June 2013, China had an overall installed capacity of 98,6 GW, almost reaching the 100 GW mark. India added 1,1 GW, a bit less than in the ¬rst half of 2013. However, considering new and ambitious plans of the new Indian government, the Indian wind market has very positive prospects.

Two other important markets, in Japan and Korea, are still growing at very modest rates, of less than 2 % in the ¬rst half of 2014. Unfortunately in both countries the nuclear lobby has still managed to prevent the breakthrough for wind power, despite the clear economic and industrial advantages.

target="_blank"

target="_blank"Europe

Germany is still the unchallenged number one wind market in Europe, with a new capacity of 1,8 GW bringing it to a total of 36,5 GW. UK (649 MW new), Sweden (354 MW new) and France (338 MW new) belong to the ¬ve biggest European markets as well, while Spain and Italy saw dramatic declines in new capacity installed, to almost zero.

The future of wind power in the Europe will also depend on decisions by the European Union regarding renewable energy targets for 2030. It is worth noting that the current crisis around Ukraine is in fact strengthening the case of renewable energy proponents, as it suggests that the European countries should increase their energy autonomy through the increased use of domestic renewable energy sources, rather than relying on imported fossil fuels.

target="_blank"

target="_blank"North America

The US market has recovered from the dramatic slump in the ¬rst half of 2013, adding 835 MW between January and June 2014, compared to 1,6 MW in the same period last year. It is expected that, due to the improved competitiveness of wind power and its increasing support, the market will further recover in the second half of 2014 and continue in 2015.

Canada installed 723 MW during the ¬rst half of 2014, 92 % more than in the same period of 2013, and has become the sixth largest market for new wind turbines worldwide. The victory of the pro-renewables proponents in the elections in the key province of Ontario gives hope that this positive tendency will continue, in spite of rather negative signals at the federal level.

target="_blank"

target="_blank"Latin America

The biggest Latin American market, Brazil, has become the 13th largest wind power user worldwide, after installing 1,3 GW in the ¬rst half of 2014 and reaching a total capacity of 4,7 GW. With a most impressive growth rate of 38,2 % during the ¬rst half of 2014, the country has become the third largest market for new wind turbines, after China and Germany, and ahead of the US and India. Brazil is expected to reach the 5 GW mark by September 2014 and to enter the list of top 10 countries with more installed capacity by the end of 2014. Other Latin American countries are emerging as wind markets as well, though at a much more modest level.

Oceania

Positive developments happened in Australia, where an additional 699 MW was installed, representing a 23% growth in comparison with end of 2013, similar to the rate of growth in 2011 and 2012. However, due to the most recent and very dramatic switch of the new Australian government, it has to be expected that this boom will not continue in the near future. No new wind farms have been registered in New Zealand.

target="_blank"

target="_blank"Worldwide prospects for end of the year 2014 and Beyond

In the second half of 2014, it is expected that an additional capacity of 24 GW will be erected worldwide , which would bring new installations for the year to 41 GW. The total installed wind capacity is expected to reach 360 GW by the end of 2014, which is enough to provide some 4 % of the global electricity demand.

The mid-term prospects for wind power investment remain positive. Although it is not clear whether the world community will be able to reach a strong climate agreement in 2015, wind has now reached a level of competitiveness and reliability, which makes it a natural option for governments, electricity producers, and consumers around the world.

posted by Herman K. Trabish @ 5:34 AM

![]()

0 Comments:

Post a Comment

<< Home