from this year’s Sustainable Energy in America Factbook:

• Total US total energy consumption rose 2.95% year-on-year as the US economy continued to rebound from the worst effects of the Covid-19 pandemic.

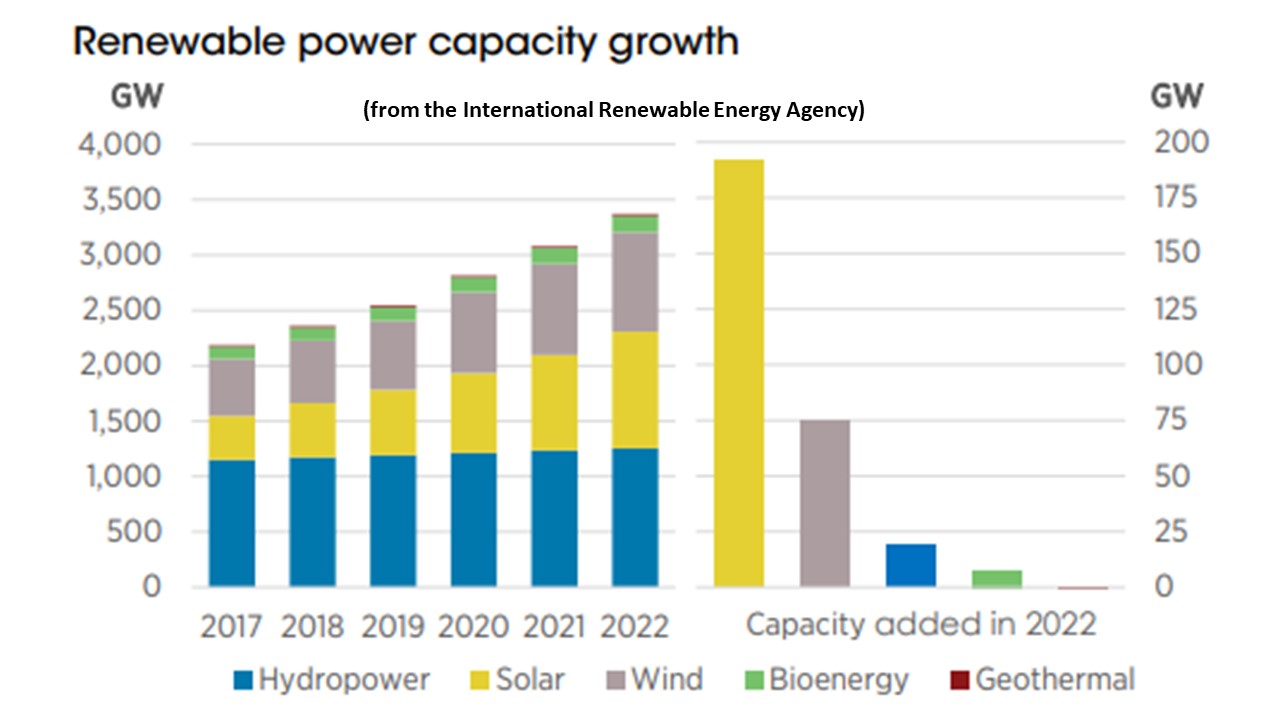

• 32GW of new renewable power-generating capacity was added to the US grid, down from 37GW commissioned in 2021. This was due to higher costs, trade challenges and other issues.

• However, renewables broke records in 2022, by meeting 13% of total US energy demand and 23% of electricity demand.

• The US remains the largest energy storage demand market in the world and commissioned an estimated 4.8GW of non-hydropower storage capacity in 2022.

• EV sales surged 50% to nearly 982,000, or 7.1% of new cars sold. This was despite rising battery costs and semiconductor shortages.

• Bucking a long-term trend, US “energy productivity” stalled slightly in 2022 as energy consumption outpaced economic growth, resulting in a 1% decline. Over a decade, however, US GDP has grown 22.9% while primary energy consumption has risen 6.7%. The result: a 15.2% increase in energy productivity.

• Corporations signed contracts to purchase a record 19.9GW of zero-carbon power, up from 17.1GW in 2021. The number of companies signing slid to 49 from 67 but deals were bigger.

• Energy spending accounted for 4.6% of total US personal consumption expenditures in 2022, up 0.63 percentage points from 2021 as fuel costs were up across the board, but still historically low.

• Demand for US natural gas rose 5.4% to reach 95.8 billion cubic feet per day. The jump was led by stronger power sector and rising LNG exports, plus modest increases across industrial, commercial, and residential sectors.

• Natural gas met 39% of US power demand with a record estimated output of 1,694MWh, up 6.5% from the year prior. Despite higher gas prices, the fuel still provided more power.

• Coal’s contribution to power generation slid to 19.4% in 2022, slightly above its recent low of 19.2% hit in 2020.

• US CO2 emissions ticked up 1.0%, BloombergNEF estimates, but were still 3% below pre-Covid levels. Transport remained the top emitting sector at 28% with power now tied with industry for next highest at 24% apiece.

• 2022 was the third most costly climate disaster year on record. The country experienced 18 climate-related disasters causing at least $1 billion in damage apiece with an $165 billion total, causing 3.4 million evacuees.

• Inflation and higher interest rates boosted levelized costs of electricity (LCOE) for most power-generating technologies in 2022, but particularly for coal and natural gas plants because of their marginal fuel costs.

• Congress passed the most consequential sustainable energy law in US history. The Inflation Reduction Act (IRA) offers at least $369 billion in support for clean energy deployment and climate action. The legislation supports multiple sectors and most of their value chains.

• Energy efficiency spending stabilized in 2021 (the last year with complete data). Utility spending on power and natural gas improvements rose 1% year-on-year to reach $7.7 billion.

• Interest in “clean” US hydrogen is growing. A total of 92MW of new electrolyzer shipments took place in 2022 but much more are expected this year. The Department of Energy has released a long-term “roadmap” for ramping hydrogen production.

• Post-IRA passage, EV and battery manufacturers raced to identify investment opportunities, with the North American battery supply chain reaching almost $17 billion by the end of 2022.

• Major oil and gas firms are upping investment in Renewable Natural Gas (RNG) in an effort to deliver “green molecules”. BP and Shell each made moves to acquire RNG producers in 2022.

A number of these trends are discussed below and all are touched on in greater depth in the Factbook’s slides.

A record-shattering year for energy transition investment

BNEF tracked over $1 trillion in global investment for technologies to decarbonize the world’s economy in 2022. The US attracted the second largest volume of new capital of any nation, with investment rising 11% year-on-year to $141 billion. Electrified transport, a category that includes revenues from the sale of EVs plus investment in charging infrastructure, was 41% of the total at $57.3 billion. Renewables accounted for 35%, down somewhat from the year prior at $49.5 billion.

The US continues to be far and away the largest market for venture capital and private equity (VC/PE) investment in start-up firms developing new technologies to address climate change. For 2022, US VC/PE totaled $25.5 billion with 422 different deals completed. The energy and transport sectors were the two best funded areas making up over half of 2022 US VC/PE investment. China was the world’s second biggest market for VC/PE, attracting $6.9 billion in 2022.

However, the level of global “sustainable debt” issued by companies and governments, often to refinance projects or issue bonds, slipped in 2022 for the first time since BNEF began tracking such data, to $1.49 trillion from $1.76 trillion a year earlier. The 15.5% decline was due to poor conditions on the public exchanges and some investor hesitancy on ESG-oriented investing. In the US, the backlash against ESG investing has grown stronger with some states even forbidding their pension fund managers to take extra-financial metrics into account in their investment processes. In the rest of the world, the fear of greenwashing has grown stronger, pushing for more regulatory developments but also placing more responsibility on financial participants to hold up to their sustainability claims.

The construction of new renewables facilities slowed, but renewables’ contributions to the grid broke records

The US added 32GW of new renewable power-generating capacity to the grid in 2022. That was down 5GW from the 37GW installed in 2021 and marked the first year-on-year slide in new build since 2018 as developers struggled with tangled supply chains and higher costs. The US solar market specifically was challenged in the first half of 2022 after the Commerce Department announced it was investigating whether to impose higher tariffs on solar equipment from four Southeast Asian nations. By June, President Biden had issued an executive order effectively postponing the imposition of any such tariffs for two years.

For wind, tax credit uncertainty, coupled with supply chain constraints, interconnection delays, and high input costs were the year’s primary complications. While the IRA revives the tax credit mechanism for new wind farms, it will take time for the support offered by the new law to translate into new capacity additions. New biomass, geothermal, waste-to-energy and small hydro capacity build remained comparatively small in 2022. In all, 21MW of new biomass and waste-to-energy capacity came online in 2022. However, for the first time, the IRA provides a more level playing field and long-term support for the full portfolio of renewable energy technologies which could impact the investment in the slower growing renewable energy sectors.

Even with the challenges, sustainable sources met a record volume of US energy demand in 2022. The contribution of renewables, including wind, solar, biomass, waste-to-energy, geothermal and hydro, rose at the fastest pace among major sectors. Renewable power jumped to 974TWh from 864TWh in 2021, a 12.6% year-on-year rise. Renewables were 22.7% of total US power generation in 2022 – its highest level ever. The growth was driven by surges in output from wind and solar and growth in hydro production.

Renewables and natural gas have grown from a combined 43% of total power generation to 62% in just a decade. In 2022, zero-carbon power (renewables generation plus nuclear power) accounted for an all-time high of 40.6% of all output. Meanwhile, coal-fired generation dipped to 19.4% of production, slightly above its recent low of 19.1% in 2020.

The process of securing all needed federal permits can be slow and laborious for energy infrastructure projects. One recent study found that the large majority of infrastructure projects take between two and six years secure all sign-offs. A quarter of such projects take longer than six years, in some cases much longer. A separate study found that renewable power projects take an average of 2-3 years to complete National Environmental Protect Act reviews specifically with a significant number of such projects taking four, five or even six years to reach completion.

US energy productivity dipped in 2022, but the long-term trend is clear

In 2022, the US economy expanded by 1.9% while primary energy consumption rose at a faster clip of 3%. Taken together, US "energy productivity" (the ratio of US GDP vs. total US energy consumption) dipped 1%. While both GDP and energy consumption rose, the former rose faster than the latter year-on-year. With Covid-19 fading, US primary energy consumption returned to pre-pandemic levels, roughly matching activity in 2019. Over the past 10 years, US GDP has grown 22.9% while primary energy consumption has risen 6.7%. The result: a 15.2% increase in productivity.

Another year of highs for US natural gas

Demand for US natural gas rose 5.4% in 2022 from the year prior to reach another record of 95.8 billion cubic feet per day (Bcf/d). The jump was led by stronger power sector consumption, rising liquified natural gas (LNG) exports, and more demand from commercial customers. The industrial and residential sectors grew more modestly. A hotter-than-normal summer and constraints on coal-fired power generation lifted use of natural gas in power. Consumption proved resilient to higher natural gas prices and the US broke seasonal demand records despite extended periods in which natural gas traded above $5 per million BTU at Henry Hub.

US exports of natural gas have risen briskly over the past decade and in 2022 LNG exports posted a 13.1% increase from the year prior to record highs. Commercial and residential demand rose on the back of the frigid start to winter 2022-23. Colder than normal weather in the second half of both November and December 2022 boosted overall consumption. Two days before Christmas, the lower-48 states set a single day record for natural gas demand.

EV sales surged

2022 was another landmark year for electric vehicles (EVs). Sales of EVs and fuel cell vehicles hit nearly 982,000, up 50% from 2021. Despite headwinds including rising battery costs and semiconductor chip shortages, EV sales surged. Tesla remained the biggest player in the market, accounting for half of new sales in 2022, but Ford, Stellantis, VW, Geely, BMW and GM also posted strong numbers. Tesla accounted for 63% of all EV sales as recently as 2020.

Battery electric vehicles (BEVs) made up 81% of 2022 sales, with plug-in hybrid electric vehicles (PHEVs) making up the remaining 19% and fuel cell vehicles accounting for under 1% of sales.

Higher prices for key clean energy commodities

Prices for key commodities that underpin the clean power sector were stubbornly high through much of 2022, but eased somewhat by year end. Polysilicon prices touched new highs in August 2022 due to temporary supply disruptions and strong demand. However, supply rose and prices fell toward the end of 2022 as existing plants returned to services and new factories were commissioned. Lithium carbonate prices spiked in 2022 and at one point the material traded at 14 times its January 2021 price. Spot prices have jumped in the past year due to high EV demand from China. By September 2022, an LFP battery cell cost $144/kWh given spot market prices for lithium carbonate, BNEF estimated. This was up 9% from November 2021 when manufacturers were just starting to see large raw material price increases. While lithium benchmarks descended slightly in December 2022, they remain at much higher levels than before the pandemic. Australia, Chile and China remain the top nations for mining lithium. The Democratic Republic of Congo remains the top producer of cobalt. Both are used in lithium-ion batteries in electric vehicles.

Elevated natural gas costs

For the second year in a row, US natural gas prices rose significantly due to tight market conditions that included rising demand for gas at home and abroad. The average benchmark Henry Hub wholesale natural gas price for the year rose 52% while residential and commercial prices rose 11% and 19%, respectively. Industrial users saw the biggest year-on-year change, with prices jumping 32%. Despite the rise, 2022 prices were still about half of those seen in 2005. Residential price adjustments tend to lag index prices 6-12 months, depending on utility practices. Industrial prices tend to be most correlated to wholesale markets. Of note, natural gas prices in the last quarter of 2022 began to decrease to below $5/MMBtu by the last week of December 2022.

US emissions ticked up, but remain below pre-Covid levels

US economy-wide emissions inched up 1.0% from 2021, BNEF estimates. This reflected the continuation of a trend begun in 2021 when the economy first began rebounding from the Covid19 pandemic. Despite the uptick, 2022 US emissions were still 3% below pre-pandemic (i.e. 2019) levels. Emissions from the transport, power, industrial and agricultural sectors of the US economy all rose but finished 2022 below 2019 levels. This suggests that some emissions reductions made in 2020 have persisted, particularly for transportation, the top emitting sector, and for the power sector that has seen steady decarbonization for the last decade due to clean generation and energy efficiency. As recently as 2016, the power sector was the number one source of US CO2 emissions. In 2022, emissions from the power sector were essentially level with those from industrial sources.

The third most costly year for climate-related disasters

The impacts of climate change continue to be felt throughout the US and 2022 was the third most costly climate disaster year on record. The country experienced 18 climate-related disasters causing at least $1 billion in damage apiece over the 12 months. Three tropical cyclones accounted for 70% of the $165 billion total. An estimated 3.4 million Americans were forced at some point to evacuate their homes during 2022 due to natural disasters, according to the Census Bureau. In response, citizens and communities are installing a growing number of residential back-up power storage systems and mini-grids.

Energy storage deployment and manufacturing

The US commissioned an estimated 4.8GW of utility-scale non-hydropower storage to bring total capacity to 11.4GW. Pumped storage is the largest energy storage resource at 67% with battery and thermal storage accounting for the rest. Despite supply-chain related delays in project development, the US remains the largest demand market for energy storage in the world. Energy shifting is the dominant use case for new batteries as pairing renewables with storage is becoming a common cost-effective option to displace fossil fuel projects. Utilities across the nation are beginning to cite energy-storage technologies in their long-term resource planning and as solutions to their power system flexibility needs.

The US also made important strides toward becoming a hub for battery manufacturing in 2022. After the IRA introduced a $45/kWh of cell and module production tax credit, automakers and battery manufacturers have raced to identify investment opportunities. Post-IRA commitments to the North American battery supply chain reached almost $17 billion by the end of 2022. A number of developers have announced plans to build or expand plants in Ohio, Michigan, Tennessee, New York and other states.

Offshore wind

The US offshore wind sector continued to make progress in 2022 with increased federal support, additional state targets and the first two commercial-scale projects under construction. However, rising equipment costs complicated some developers’ plans. Critically, the IRA extended the Investment Tax Credit (ITC) for offshore wind until at least 2032, allowing developers to reduce their projects’ building costs potentially by 30%. The Bureau of Ocean Energy Management (BOEM) held three lease auctions in 2022. At the state level, California, Louisiana, and New Jersey all either created or expanded offshore wind targets.

The most important federal energy transition investment in US history

In a surprise turn of events in August, Congress passed the IRA, the most consequential law ever intended to address climate issues. The law represented a major victory for various clean energy sectors. The IRA provides at least $369 billion in support to energy transition technologies. The law primarily uses tax credits to achieve its goals, estimated at least at $271 billion, over a tenyear time horizon. It extends or expands credits for virtually every energy transition sector, with a transition to a technology-neutral approach for many after year two. Within each major sector, it offers support from the bottom to the top of the value chain, from end consumers up to raw materials providers.

The law stands to put the US far closer to the Biden administration goal of halving economy-wide CO2 emissions by 2030 (vs. 2005). The Treasury Department is in the process of writing many of the rules in 2023 on how these and other tax policies are implemented.

Interest in “clean” hydrogen grows with IRA passage

Today, the US consumes approximately 10 million metric tons of conventional hydrogen annually in industries such as oil refining and ammonia production. These industries, along with others like steel production and energy storage, could shift the US from carbon-intensive hydrogen consumption to low-carbon hydrogen consumption in the coming years. In 2022, BloombergNEF tracked 92MW of hydrogen-producing projects commissioned. A more diverse slate of players is now poised to get involved in production. SolCaGas announced the Angeles Link project in 2022, a green hydrogen production pipeline serving the Los Angeles region – anticipated to be the nation’s largest. In 2023, CF Industries Inc. is expected to commission an electrolyzer at a large ammonia production facility. Air Products and Chemicals Inc. plans to commission an electrolyzer focused on road transport. Florida Power and Light seeks to commission a facility to generate power. RNG is also attracting new interest and investment, stemming from new incentives for RNG production from the IRA.

Energy efficiency spending stabilized after a Covid-related drop

After a sharp drop in efficiency spending from 2019 to 2020 due to the pandemic, efficiency spending stabilized in 2021 (the last year for which there is complete data). Spending rose 1% year-on-year from 2020 to 2021 to reach $7.7 billion, according to data compiled by the American Council for an Energy Efficient Economy (ACEEE). Spending on efficiency improvements related to electricity only stayed essentially flat at $6 billion in 2021 while spending on improving the efficiency of natural gas delivery grew from $1.5 billion to $1.7 billion. The total impact of all ratepayer-funded electric energy efficiency programs in place in 2021 was a savings of about 290 million MWh– equivalent to approximately 7.63% of 2021 electricity consumption, according to ACEEE…

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

Plug-in Hybrids, The Cars That Will Recharge America

Plug-in Hybrids, The Cars That Will Recharge America Oil On The Brain

Oil On The Brain