Towards an Accessible Financing Solution; A Policy Roadmap With Program Implementation Considerations For Tariffed On-Bill Programs In California

Bruce Mast, Ardenna Energy, LLC Holmes Hummel, Clean Energy Works Jeanne Clinton, July 20, 2020 (Building Decarbonization Coalition)

Executive Summary

Introduction to the Executive Summary

California has established the ambitious climate protection goal of achieving full carbon neutrality by 2045 and to do so in a way that supports the health and economic resiliency of urban and rural communities, particularly low income and disadvantaged communities. To achieve this goal, the residential building sector, along with every other sector, must reach zero emissions, including greenhouse gases (GHGs) from fossil-fuel end uses. To achieve building decarbonization at scale, California will need an artful combination of updated building codes, appliance standards, regulatory requirements, public funding, and ratepayer-funded incentives, combined with policies and programs that overcome long-standing upfront cost barriers that deter households from making cost-effective clean energy investments.

California also needs an equitable emissions reduction strategy. If we are to reach the state’s policy objectives, a building decarbonization strategy must be robust enough to enable the participation of California’s low- and moderate-income (LMI) and renter households, who together represent more than 40 percent of the state’s population. California must identify the means to overcome the upfront cost and split incentive barriers in order to put decarbonization investments within reach of all Californians, regardless of income, credit history, liquidity, or home ownership status. As signatories to the Equitable Building Electrification framework pointed out, Environmental and Social Justice (ESJ) communities “…are likely to be left using gas if market forces are the primary driver of electrification.”1 A grant-only approach to LMI building decarbonization investments would require a cumulative 25-year public and ratepayer capital commitment on the order of $72–150 billion. This level of spending on building decarbonization would dwarf any public expenditure the state of California has made for energy efficiency or renewable energy programs. One can thus infer that exclusive reliance on grant-only programs leaves ESJ communities at risk of getting left behind.

The Building Decarbonization Coalition launched the Accessible Financing Project to address these barriers and expand access to clean energy upgrades with a combination of funding and financing. The Project goal was to develop a policy roadmap for opening the clean energy economy to LMI households and renters, specifically in the realm of upgrades that decarbonize buildings. In the course of stakeholder engagement, it became evident that there was strong interest in wading further into issues of due diligence and implementation. Our recommendations will outline a path to address all three dimensions.

While our focus is on identifying solutions to barriers faced by LMI households and renters, it is not our intent to limit the recommended finance solution to these customer segments. Our overarching goal remains an accessible financing solution that is universally accessible to all California households, without regard to income level. Our belief is that a solution that works for the most challenging use cases (LMI households and renters) will also expand accessibility for easier use cases (e.g., higher-income property owners).

We also note that a financing mechanism need not replace or diminish existing grant or free direct-installation programs for lower income residents. Combining grants with accessible finance mechanisms can expand overall access and participation. This approach will accelerate adoption of more comprehensive investments in building energy upgrades, and thus leverage public funding with financed investment for greater impact.

To effectively address upfront cost and split incentive barriers, and to support the scale of investment state policy requires, we defined the following design criteria as benchmarks of success:

1. Ability to finance over long periods (10–15 years) even in rental units with multiple changes in tenancy

2. Ability to leverage utility bill savings to defray investment costs, rather than rely on consumer credit or home equity

3. Cash-positive outcomes that assure LMI customers will not experience increased energy burdens

4. Ability to scale to serve millions of California households

A threshold research finding that guided the Project’s subsequent investigations is that consumer credit finance products are ill suited to meet the design criteria above. This knowledge already has motivated multiple public agencies to develop policy recommendations and solutions that would facilitate site-specific clean energy investments with utility or societal capital and site-specific cost recovery consistent with regular terms of service offered by utilities. This approach offers three key benefits that align directly with Project design criteria:

• Assigning the capital commitment to a site (e.g. home, condominium, or apartment through its utility meter), rather than to an individual, avoids the need for consumer credit risk screening that would otherwise disqualify more than one third of all consumers based on income, credit score, or renter status.

• Leveraging a utility’s existing mechanisms for making utility capital investments with cost recovery through monthly bills allows a single utility bill to combine decarbonization investment service costs for “behind-the-meter” improvements with the lower utility bills resulting from the improvements made.

• The level of uncollected revenue on expected utility bill payments (i.e. charge-off rate) is typically low compared to much higher default levels on consumer debt instruments, making cost recovery via the utility bill attractive and lower risk. Consistent with those policy recommendations, the BDC Accessible Financing Project research team prioritized attention to the potential to address the key design requirements with site-specific investment and cost recovery through utility tariffed on-bill programs.

Combining Multiple Value Streams to Mobilize Investment

While some residential decarbonization investments in California will produce positive bill savings with current market conditions, this is not true for all of our state’s housing stock today, even if the value proposition continues to improve over the next decade. For many, the savings based on current energy prices and equipment costs will be too modest to cover the full investment cost and, for others, such as those living in moderate climate zones, the savings may not cover even the incremental costs. Yet our state’s climate goals dictate that we achieve zero emissions in the housing sector. This dilemma requires a broader economic lens to recognize the total value of clean energy investments accruing to different stakeholders, and then striving to both align and combine the multiple value streams.

Conceptually, utility bill savings alone need not cover the full cost of clean energy investments. While the total cost of many building decarbonization upgrades are not cost effective by leveraging customer bill savings alone, some portion of every decarbonization upgrade would meet the cost effectiveness criteria for a tariffed on-bill investment. This means that building decarbonization upgrades require a combination of financing for the portion of the upgrade costs that can be recovered from bill savings, and other co-funding associated with one or more of the additional value streams:

1. Customer co-benefits. It is reasonable to expect occupants (owners and renters) to harness the value of any additional benefits experienced beyond utility bill savings (such as better health, lower health care costs, increased comfort, etc., which are considered “co-benefits”) with a co-pay that captures some of the value of these co-benefits.

2. Societal costs and benefits. To the extent that net societal costs and benefits of decarbonization are positive yet not already reflected in retail energy prices, public funding sources should contribute to those decarbonization investments.

3. Grid operator costs and benefits. Decarbonization activities that reduce utility system delivery costs, improve grid flexibility to balance intermittent generation sources, or enhance system performance can produce value streams that harness the motivation to invest. For example, the value of avoided costs to the gas distribution system and the associated grid co-investments may be higher when whole communities (or all buildings served by a single distribution branch) decarbonize at one time.

4. Landlord-tenant equity. Co-payments by landlords for some of the cost of replacing heating, cooling, and water heating equipment could be considered a core co-funding requirement, in keeping with their fiduciary responsibility to provide space heating and hot water.

Overview of Existing Tariffed On-Bill Programs

Tariffed on-bill programs based on the PAYS® (Pay As You Save®) 2 system have been successfully implemented during the past 18 years in eight states by 18 utilities from Hawaii to New Hampshire, including investor owned, cooperative, and municipal utilities. More than $30 million has been invested in energy efficiency and renewable upgrades at 5,000 locations.3 Utilities that have experience offering tariffed on-bill programs have reported results that indicate consistently high adoption rates for building energy efficiency upgrades and low charge-off rates for nonpayment, even in areas characterized by conditions of persistent poverty.

In 2019, U.S Department of Energy (DOE) released an Issue Brief on the topic of tariffed on-bill programs through its Better Buildings Solutions Center. Below is an adapted excerpt:

A tariffed on-bill program allows a utility to pay for cost-effective energy improvements at a specific residence, such as home heating and cooling units, and to recover its costs for those improvements over time through a dedicated charge on the utility bill that is immediately less than the estimated savings from the improvements.

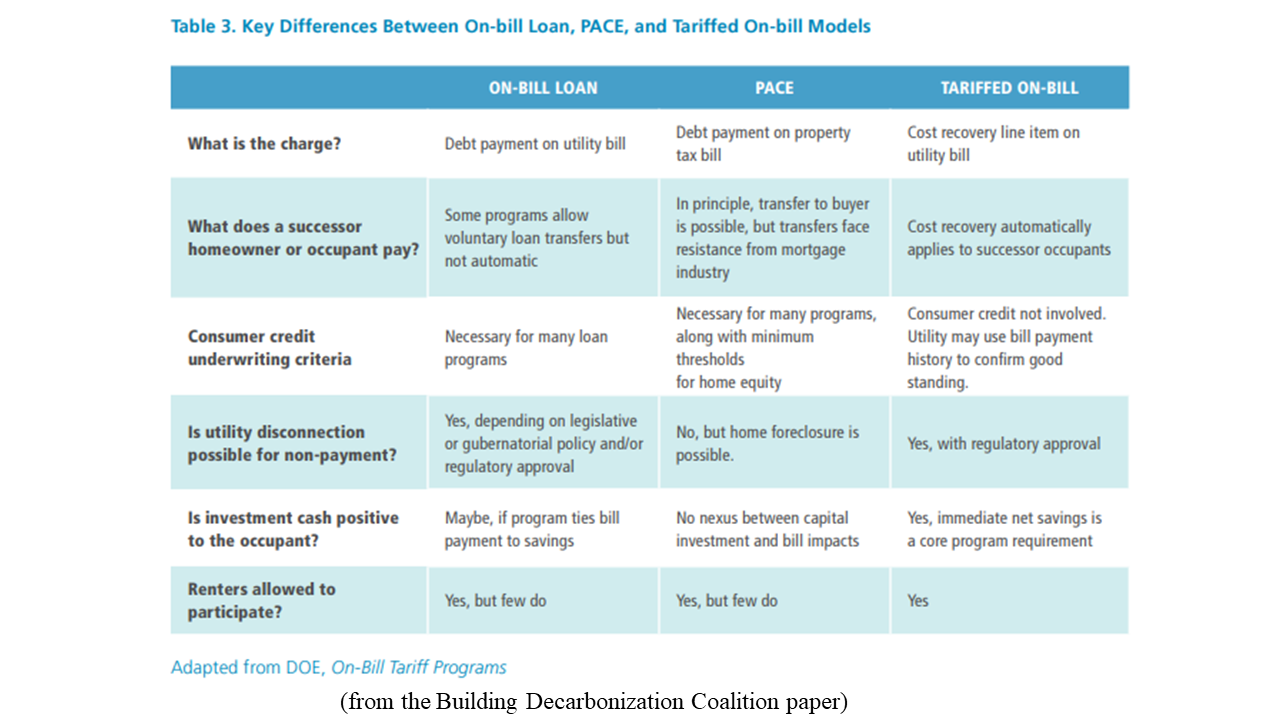

The tariffed on-bill model differs from on-bill loans and repayment models in that tariffs are not a loan, but rather a utility investment for which cost recovery is tied to the utility meter according to terms set forth in a utility tariff.5

A tariff (or tariff rider) approved by utility regulators sets forth the terms of service for an investment made at a single location, with the cost recovery assigned only to the meter at that location. The tariff charge will remain attached to the meter at the improved location, regardless of who occupies the property, until utility cost recovery is complete.

The tariffed on-bill upgrade is associated with the utility meter location, not an individual household account. Therefore, utilities do not have to evaluate occupant credit scores and debt-to-income ratios, nor screen participants for homeownership status.

Because there is no customer debt obligation, the terms in the tariffed on-bill program apply automatically to the current customer as well as future customers at each upgraded location. The tariffed charge for cost recovery of the utility expenditure survives foreclosure proceedings, changes in tenancy, and can be floated through periods of vacancy.

Residents pay utility bills that are lower than they would have been without the upgrades and, if designed with consumer protections in place, the energy savings are greater than the tariff charge that recovers the utility investment. This reduces risk to residents, who, if they used on-bill financing or repayment, might otherwise have been forced to pay off their debt if they wished to move before the loan repayment was complete.

The on-bill tariff program is especially good for removing barriers to rental home upgrades because the program enables a utility to recover its cost for energy improvements even if [initial] renters leave before the recovery is complete.

Near-Term Pathway to Tariffed On-Bill Programs

Our assessment of the current regulatory environment in California is that publicly owned utilities (POUs) and investor-owned utilities (IOUs) already have broad discretion to implement tariffed on-bill programs, subject to review and approval by their governing board, in the case of POUs, or by the California Public Utilities Commission (CPUC) in the case of IOUs. The CPUC and POU governing boards have the authority to authorize:

• utility investments of capital

• public purposes to be served by utilities regarding energy, related environmental dimensions including greenhouse gases (GHGs), and customer health, safety, and comfort

• rules for utility procurement and deployment of capital, infrastructure, and services

• billing mechanisms and tariffs

For IOUs, a rate case application is considered and authorized by the CPUC for cost recovery of the total amount of investment and capital required, including authorized rate of return on equity and debt. Utility tariffs describe the details of cost recovery via service charges on affected customers’ bills.

POUs have autonomy to enact comparable tariffs, subject to review and approval by their governing boards. Two California local governments (Town of Windsor and the City of Hayward) have used their public water utility capital sources and billing systems to administer Pay As You Save® efficiency programs that mirror many of the features of the tariffed on-bill model we address here.

Community Choice Aggregators (CCAs) in California are currently not authorized to initiate tariffed on-bill programs because no California electric or gas utility is yet approved to make site-specific investments through a tariff that assigns cost recovery to a location rather than a customer.6 In accordance with current California policies, only distribution utilities are permitted to disconnect customers for non-payment for an essential utility service, and no electric or gas utility regulator has yet determined that site-specific energy upgrades such as energy efficiency and building decarbonization are essential utility services. With such approval, a utility could partner with one or more CCAs to serve as a program operator to coordinate local implementation of the investment program.

We recommend that POUs and IOUs move expeditiously to secure necessary approvals for the design and launch of tariffed on-bill programs for building energy upgrades that could include building decarbonization, energy efficiency, and more. Specifically, the CPUC and POU governing boards should follow a three-stage approach, starting with establishing a policy framework, then proceeding to due diligence, and then providing direction on implementation.

Establish Policy Framework

CPUC and POU governing boards should provide enabling direction that sets in motion the program due diligence and planning process. This phase involves establishing threshold regulatory policies that establish tariffed on-bill programs as permissible. It also sets parameters for the scope of due diligence required for select program design elements, notably consumer protections and capital sources. Regulators should:

1. Authorize utilities to deploy capital and recover cost for building decarbonization upgrades via tariffed on-bill structures that enable participation regardless of income, credit score, or renter status

2. Authorize utilities to make these “behind the meter” investments on terms that assure a path to ownership for customers while also assuring full cost recovery with a return on utility investment, on par with conventional utility investments

3. Direct that tariffed on-bill payments be treated as a regular element of utility tariffs and bill payment, subject to customary procedures and notices should there be payment arrears

4. Establish minimum thresholds for consumer protections 5. Establish guidelines for source capital, considering implications for utility balance sheets and access to broader capital markets

Due Diligence And Feasibility

While this White Paper attempts to provide guidance on key implementation issues, a comprehensive due diligence and feasibility analysis is beyond the scope of this effort. Toward that end, regulators should allocate resources to investigate economics and cost allocations, financial and legal risks, and stakeholder roles and responsibilities. This phase should address the following critical issues:

Economics and Cost Allocations

1. Conduct economic potential study encompassing full span of potential decarbonization investments on the customer side of the meter; quantify expected societal benefits from promising decarbonization packages; incorporate current assumptions about future rate increases, transition to time-of-use (TOU) rates, net energy metering (NEM), and CARE discounts into customer economic analysis

2. Analyze financial implications of assigning indirect costs (e.g., cost of capital, program administration, measurement and verification (M&V), loss reserves) to participating customers versus ratepayers

3. Investigate information system requirements and associated capital investments to support customer billing under different risk-reward allocation scenarios

4. Assess market potential for decarbonization packages offering attractive customer economic benefits; incorporate analysis of customer-specific Advanced Metering Infrastructure (AMI) data to inform customer segmentation and estimate potential investment contributions from customer energy cost savings; estimate supporting incentive and customer co-pay requirements, including landlord co-pays for rental housing retrofits.

Financial and Legal Risks

5. Perform risk analysis, including perspectives of current and successor customers, ratepayers, program sponsors, energy services companies and other private-sector service providers, and capital providers

6. Identify consumer protection mechanisms that balance costs, risks, and rewards, and authorize mechanisms to mitigate the potential for above-normal costs to ratepayers from unpaid bills (e.g. reserve funds).

7. Investigate options for source capital, supported by strong assurances of repayment

8. Evaluate potential jurisdictional issues that could be brought up around liability and property law; determine appropriate legal framework for ownership of investment assets

Roles and Responsibilities for Program Offerings

9. Articulate possible roles for POUs and CCAs

10.Establish ground rules for program sponsors to obtain access to customer-specific gas and electricity consumption, including whole-building consumption data for multifamily facilities

11.Authorize third parties to take on responsibility for customer utility bill payments

As part of due diligence activities above, the research team should conduct active stakeholder engagement, with particular attention to ESJ communities, prospective capital providers, and private sector service providers.

Based on due diligence outcomes, regulators should provide guidance on:

1. Performance metrics for program success, considering potential metrics such as default or charge-off rates, market share, participant demographics, contribution to customer wealth building, economic performance, GHG emissions reductions, other social outcomes

2. Scope of decarbonization measures and criteria for integrating multiple funding sources

3. Assignment of indirect costs (e.g., cost of capital, program administration, M&V, loss reserves) to participating customers versus ratepayers, leading to authorized funding from ratepayer sources

4. Program parameters, including consumer protection mechanisms, capital sources, and risk allocations

Implementation

Based on the blueprint established through the due diligence process, program sponsors should be empowered to design and implement programs, including:

1. Conduct market research to assess optimal methods for communicating program costs, risks, and rewards to consumers

2. Develop customer acquisition strategies and phased roll-out plan

3. Establish detailed implementation plans

Longer-Term Policy Roadmap for Achieving Scale and Meeting Climate Goals

The scale and speed of investments required to meet the state’s climate action goals dictate an emphasis on scalable solutions capable of attracting substantial private investment. The near-term policy pathway described above should provide critical early momentum. Additional policy developments should focus on accelerating that momentum.

Parallel implementation of what could be multiple local and regional tariff on-bill programs does not automatically lead to a scalable statewide solution that would be attractive to large-scale capital providers. To avoid fragmented solutions, policy development should focus on two issues:

1. Combine public investments in related decarbonization strategies (e.g., energy efficiency, electrification, rooftop solar, and on-site energy storage) and align program policies and procedures to capture larger total value streams for integrated projects. For example, more efficiency and electrification investments can be achieved when combined with the cash flows of on-site solar projects. Combining multiple value streams, including tariffed on-bill investment, will expand the number of financially viable decarbonization projects.

2. Move towards integrated statewide program administration and implementation to enable large aggregated investment portfolios and the associated economies of scale in securing capital and managing overhead costs.

Recommendations For Enabling Large Scale Capital Deployment For Building Decarbonization…

Recommendations For Statewide Program Administration…

Time is a critical factor in capitalizing tariffed on-bill investments at a scale sufficient to achieve California’s policy objectives. While these recommendations may be taken up in any order, near-term pathway actions by utilities and utility regulators are critical to getting started at an initial scale. Supporting actions by the state legislature and governor can accelerate implementation…

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

Plug-in Hybrids, The Cars That Will Recharge America

Plug-in Hybrids, The Cars That Will Recharge America Oil On The Brain

Oil On The Brain