Climate Change Vulnerability Study

December 2019 (Consolidated Edison)

Executive Summary

In its 2013 rate case filing after Superstorm Sandy, Con Edison proposed $1 billion in storm hardening investments to build additional resiliency into its energy systems. Con Edison worked with a Storm Hardening and Resiliency Collaborative to recommend optimal investments for the proposed storm hardening funds, including the recommendation that Con Edison conduct a Climate Change Vulnerability Study (Study). As described by the New York State Public Service Commission, the purpose of this Study is to aid in the ongoing review of the Company’s design standards and development of a risk mitigation plan.1 Over the course of the Study, Con Edison regularly convened a stakeholder group to provide feedback, consisting of many of the same participants from the Storm Hardening and Resiliency Collaborative. The findings from the Study equip Con Edison with a better understanding of future climate change risks and strengthen the company’s ability to more proactively address those risks.

This Study describes historical and projected climate changes across Con Edison’s service territory, drawing on the best available science, including downscaled climate models, recent literature, and expert elicitation. Con Edison recognizes the global scientific consensus that climate change is occurring at an accelerating rate. The exact timing and magnitude of future climate change is uncertain. To account for climate uncertainty, the Study considered a range of potential climate futures reflecting both unabated and reduced greenhouse gas concentrations through time and evaluated extreme event “stress test” scenarios.

This Study evaluates present-day infrastructure, design specifications, and procedures against expected climate changes to better understand Con Edison’s vulnerability to climate-driven risks. This analysis identified sea level rise, coastal storm surge, inland flooding from intense rainfall, hurricane-strength winds, and extreme heat as the most significant climate-driven risks to Con Edison’s systems. Con Edison has unique energy systems, and vulnerabilities vary across those systems. The utility’s electric, gas, and steam systems are all vulnerable to increased flooding and coastal storms; workers across all commodities are vulnerable to increasing temperatures; and the electric system is also vulnerable to heat events.

While Con Edison already uses a range of measures to build resilience to weather events, the vulnerabilities identified in this Study guide the company to pursue additional strategies to mitigate climate risks. The Study establishes an overarching framework that can work to strengthen Con Edison’s resilience over time. While many adaptation strategies focus on avoiding impacts altogether, a comprehensive resilience plan also requires a system that can reduce and recover from impacts, particularly following outages.

Over the course of 2020, Con Edison will develop and file a Climate Change Implementation Plan, which will specify a governance structure and a strategy for implementing adaptation options over the next 5, 10, and 20 years. While this Study assesses vulnerabilities within Con Edison’s present-day systems to a future climate, the implementation plan must also consider the evolving market for energy services, and potential changes to services and infrastructure driven by customers, government policy and external actions over time.

The Need for a Study

The New York State Public Service Commission approved an Order and funding for Con Edison to conduct a Climate Change Vulnerability Study, with a requirement for delivery by the end of 2019. The Con Edison Department of Strategic Planning undertook this Study with support from more than 100 subject matter experts throughout the company and in collaboration with ICF’s climate adaptation and resilience experts and Columbia University’s Lamont-Doherty Earth Observatory. The Study was designed to meet three primary goals:

1. Research and develop a shared understanding of new climate science and projected extreme weather for the service territory.

2. Assess the risks of potential impacts of climate change on operations, planning, and physical assets.

3. Review a portfolio of operational, planning, and design measures, considering costs and benefits, to improve resilience to climate change.

A New Understanding of Climate Science and Extreme Weather

Con Edison will face new challenges from a rapidly changing climate through the 21st century. To better understand these challenges, the Study characterized historical and projected changes to climate hazards within the service territory to estimate the magnitude and timing of potential climate vulnerabilities. Climate variables that present outsized impacts to Con Edison include temperature, humidity, precipitation, sea level rise, and extreme events, such as rare hurricanes and long-duration heat waves…Temperature…Humidity…Precipitation…Sea Level Rise…Extreme Events…

Characterization of Con Edison’s Vulnerabilities to Climate Risks

Heat and Temperature Variable

The core electric vulnerabilities to increasing temperature and TV include increased asset deterioration, decreased system capacity, increased load, and decreased system reliability. Since the internal temperature of electric power equipment is determined by the ambient temperature as well as the power being delivered, higher ambient temperatures increase the internal operating temperature of equipment…

Flooding from Precipitation, Sea Level Rise, and Coastal Storms

All underground assets are vulnerable to flooding damage (i.e., water pooling, intrusion, or inundation) from precipitation events, sea level rise, and coastal storms. Following Superstorm Sandy in 2012, Con Edison protected all infrastructure in the floodplain against future 100-year storms and 1 foot of sea level rise (e.g., submersible infrastructure, flood walls, pumps, elevation). Sea level rise projections suggest that Con Edison’s 1 foot of sea level rise risk tolerance threshold may be exceeded as early as 2030 and as late as 2080…

Extreme and Multi-Hazard Events

The Study team reviewed the vulnerabilities of Con Edison’s electric, gas and steam systems to future extreme events based on specific, worst case extreme event narratives (Category 4 hurricane, a strong nor’easter, and a prolonged heat wave) designed to stress-test these systems.

Storm surge driven by an extreme hurricane event (i.e., a Category 4 hurricane) has the potential to flood both aboveground and belowground assets. In addition, wind stress and windblown debris can lead to tower and/or line failure of the overhead transmission system and damage overhead distribution infrastructure, which could cause widespread customer outages…

Resilience Management Framework

To conceptualize how to systematically address vulnerabilities, the Study team developed a resilience management framework (Figure 2). The framework encompasses investments to better withstand changes in climate, absorb impacts from outage-inducing events, recover quickly, and advance to a better state. The “withstand” component of this framework prepares for both gradual and extreme climate risks through resilience actions throughout the life cycle of the assets. As such, many adaptation strategies fall under this category. Investments to increase the capacity to withstand also provide critical co-benefits such as enhanced blue-sky functionality and reliability of Con Edison’s systems. The resilience management framework facilitates long-term adaptation and creates positive resilience feedback so that Con Edison’s systems achieve better functionality through time. To succeed, each component of a resilient system requires proactive planning and investments.

Adaptation Measures to Address Vulnerabilities

Con Edison has already undertaken a range of measures to increase the resilience of its systems. For example, lessons learned and vulnerabilities exposed during past events, including Superstorm Sandy (2012) and the back-to-back nor’easters (winter storms Riley and Quinn, 2018), resulted in significant capital investments to harden the system. Looking forward, as Con Edison is investing in the system of the future—one with greater monitoring capabilities, flexibility, and reliability—it is simultaneously building a system that is more resilient to extreme weather events and climate change. In addition to new investments, Con Edison also conducts targeted annual updates to its system to ensure capacity and reliability, which help the company keep pace with recent changes in temperature and humidity.

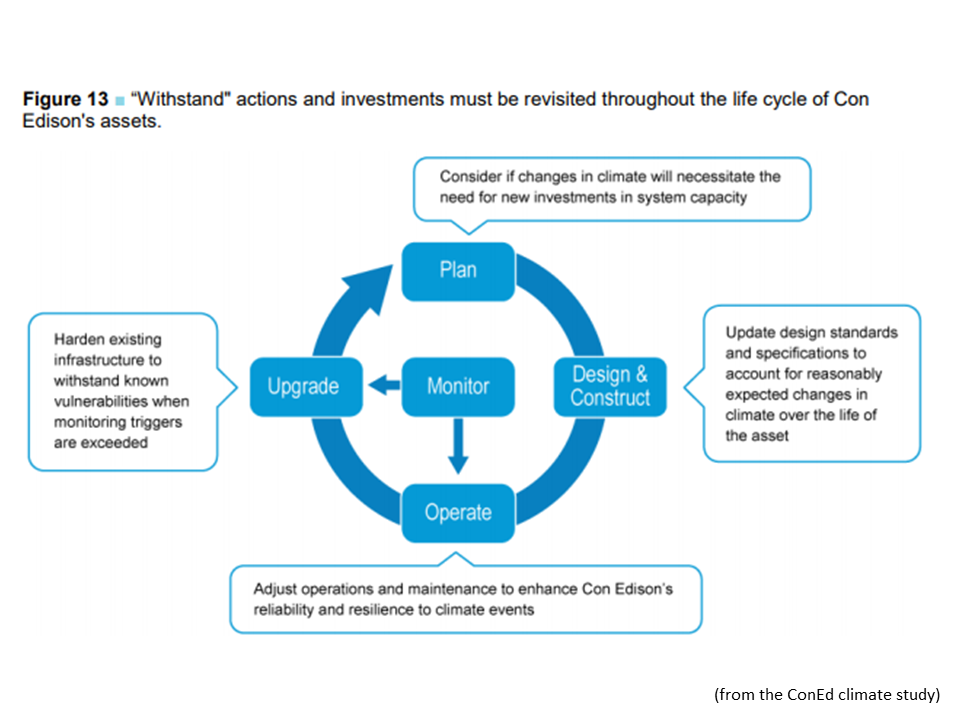

Withstand Gradual Changes in Climate and Extreme Events

Resilience actions should occur systematically throughout an asset’s life cycle to enhance the ability to withstand changes in climate while also enhancing system reliability and blue-sky functionality. This can be accomplished through planning, designing, and upgrading assets in a resilient manner, with ongoing monitoring throughout.

Plan

Incorporating climate change projections into Con Edison’s routine planning processes will help identify capital needs and help the systems gradually adjust to changes in climate. Some of the types of planning processes and tools that may benefit from consideration of climate change include the following:

• Load and volume forecasting for all commodities

• Load relief planning for the electric system, which should include reduced system capacity and higher load due to warmer temperatures

• Working with utilities in other environments to understand how they plan and design their system for the climate Con Edison will experience in the future

• Long-range planning for all commodities

• Network reliability modeling and planning

Design

The key to designing resilient infrastructure is to update design standards, specifications, and ratings to account for likely changes in climate over the life cycle of the infrastructure. While there is uncertainty as to the exact changes in climate an asset will experience, selecting an initial climate projection design pathway allows engineers to design infrastructure in line with Con Edison’s risk tolerance. The Study team suggests an initial climate projection design pathway that follows the 50th percentile merged RCP 4.5 and 8.5 projections for sea level rise and high-end 90th percentile merged RCP 4.5 and 8.5 projections for heat and precipitation.

Upgrade

Changing design standards will influence the construction of new assets but does not address the vulnerability of existing assets. A flexible and adaptive approach to managing and upgrading assets will allow Con Edison to manage risks from climate change at acceptable levels, despite uncertainties about future conditions. The flexible adaptation pathways approach allows Con Edison to adjust adaptation strategies as more information about climate change and external conditions that may affect Con Edison’s operations is learned over time. Figure 3 depicts how flexible adaptation pathways are based on flexible management to maintain tolerable levels of risk.

As conditions change over time, Con Edison will need to consistently track these changes to identify when decision making for additional or alternative adaptation strategies is required. This approach relies on monitoring indicators, or “signposts,” that provide information which is critical for adaptive management decisions. Broad categories of signposts that Con Edison should consider monitoring include climate variable observations and best available climate projections; climate impacts; and policy, societal, and economic conditions. Predetermined thresholds for these conditions signal the need for a change in action, which support decisions on when, where, and how Con Edison can take action to continue to manage its climate risks at an acceptable level…

Absorb and Recover from the Impacts of Extreme Events

It is neither efficient nor cost-effective for Con Edison to harden its systems to withstand every type of extreme event. Instead, Con Edison must use a broader suite of adaptation strategies to absorb and recover from the inevitable disruptions caused by extreme events exceeding their design standards. Con Edison currently incorporates “absorb” into its design and operations with, for example, a limited ability to control customer demand and shed load in extreme cases. A broader suite of strategies focuses on emergency preparedness, limiting customer impact and improving customer coping, including the following:

• Supporting the creation of resilience hubs (spaces that support residents and coordinate resources before, during, and after extreme weather events (Baja, 2018) and have continued access to energy services)

• Using smart meters to implement targeted load shedding to limit the impact to fewer customers during extreme events

• Strengthening staff skills for streamlined emergency response

• Planning for resilient and efficient supply chains

• Coordinating extreme event preparedness plans with external stakeholders

• Incorporating low-probability events into long-term plans

• Expanding extreme heat worker safety protocols

’

• Examining and reporting on the levels of workers necessary to prepare for and recover from extreme climate events

• Investing in energy storage, on-site generation, and energy efficiency programs

Advance

Advancing to a better adapted, more resilient state after an outage-inducing event (i.e., building back better/stronger) begins with effective pre-planning for post-event reconstruction. Even with proactive resilience investments, events can reveal system or asset vulnerabilities. Where assets need to be replaced during recovery, having a plan already in place for selection and procurement of assets designed to be more resilient in the future can help to ensure that Con Edison is adapting to a continuously changing risk environment. Outage-inducing events also provide important opportunities to measure the performance of adaptation investments, helping to inform additional actions that further resilience.

Next Steps

As a next step from this Study, Con Edison will develop a detailed Climate Change Implementation Plan to integrate the recommendations from this Climate Change Vulnerability Study. The implementation plan will be developed in close coordination with Con Edison SMEs and will utilize quarterly meetings with external stakeholders. The implementation plan will consider updates in climate science, finalize an initial climate design pathway, integrate that pathway into company specifications and processes based on input from subject matter experts, develop a timeline for action with associated costs and signposts, and recommend a governance structure. Some key items for consideration in the implementation plan include determining the appropriate amount of proactive investment, changes in the policy/regulatory and operating environment and the establishment of a reporting structure…

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

Plug-in Hybrids, The Cars That Will Recharge America

Plug-in Hybrids, The Cars That Will Recharge America Oil On The Brain

Oil On The Brain