TODAY’S STUDY: THE NEW ENERGY FACTS NOW

Sustainable Energy In America Factbook 2015 Executive Summary

February 2016 (Bloomberg New Energy Finance)

Overview

Two thousand fifteen will surely be remembered as a watershed year in the evolution of US energy, as the industry passed important milestones and the federal government finalized critical new policies. The already rapid de-carbonization of the US power sector accelerated with record numbers of coal plant closures and solar photovoltaic system commissionings, while natural gas production and consumption hit an all-time high. Concurrently, the US continued to enjoy greater benefits from energy efficiency efforts as economic growth outpaced the growth in electricity consumption.

The net result on the planet: US power sector CO2 emissions fell to their lowest annual level since the mid-1990s. The net impact on consumers: negligible to positive as prices for electricity and fuel remained low by historic standards and customer choices expanded. Perhaps most importantly, many of the key changes seen in 2015 are likely permanent shifts, rather than temporary adjustments due to one-time events.

On the policy front, major initiatives appear poised to keep the US on track toward de-carbonization in the coming decades. In August, the Obama administration finalized its Clean Power Plan regulation for the existing US power fleet. In December, the US joined with 194 other nations in France to adopt the “Paris Agreement” which includes pledges to rein in emissions over the coming decades. The year closed with Congressional approval of a major, five-year extension of key tax credits supporting new US wind and solar projects and a two-year extension of measures supporting energy efficiency. The Production Tax Credit (PTC) was also extended to cover geothermal, biomass, waste-to-energy, landfill gas, hydro and ocean energy projects that commence construction before 2017.

As in years past, the goal of the 2016 Factbook is relatively simple: to record and highlight the important developments that transpired in US energy over the prior 12 months. It also provides a look back over the past seven years, and in some cases decades, to show trends. Among the most notable developments:

click to enlarge

click to enlarge• Investment in energy efficiency continues to pay dividends for the US economy.

– Energy productivity – the ratio of US GDP to energy consumed

– continues to grow, improving by 2.3% from 2014 to 2015 following a 1.1% increase the previous year. The US economy has now grown by 10% since 2007, while primary energy consumption has fallen by 2.4%. And while the shifting composition of the US economy is no doubt a driver, estimates put forward by the American Council for an Energy Efficient Economy indicate that as much as 60% of the energy intensity improvements seen since 1980 are due to efficiency gains, with only 40% the result of structural changes in the US economy.

– Within the electricity sector specifically, this “decoupling”

– a disconnection between energy consumption and economic growth

– is also visible: electric load growth in 2015 clocked in at only 0.5%, compared to a projected 2.4% increase in GDP. And since 2007, electricity demand has been flat, compared to a compounded annual growth rate of 2.4% from 1990 to 2000.

– Meanwhile, final data for 2014 – the latest year for which we have estimates

– show that annual investment in energy efficiency measures continues to grow. Natural gas and electric utility spending on efficiency reached $6.7bn, up 8.1% from the $6.2bn seen in 2013; Energy Savings Performance Contracting (ESPC) investment topped $6.4bn. Accordingly, electricity savings continue to climb year-on-year, breaching 25GWh in 2015. Since 2007, incremental efficiency achievements have risen 17% on average annually. On a sectoral basis, efficiency investment shrank slightly in the residential sector for the first time in over a decade, but expanded in commercial, industrial and other sectors. Regionally, New England, the Pacific, Great Lakes and the Mid-Atlantic region still lead in electrical efficiency savings. The Southeast remains a largely untapped market with fewer enabling policies such as energy efficiency resource standards (EERS).

click to enlarge

click to enlarge• The US is making major strides toward a de-carbonized electricity grid and set important new records in 2015. Critically, these milestones represent structural changes to the fleet, suggesting a permanent change is afoot.

– Challenging economics and the shadow of environmental regulations encouraged the accelerated retirement 14GW of coal-fired power plants, representing 5% of the installed coal capacity in the country. Since 2005, the US has disconnected over 40GW of coalburning power plants, while adding only 19GW new coal to the grid. Several gigawatts of coal-fired capacity have also converted to natural gas or, in a few cases, biomass. Due to both these retirements and competition from low-priced natural gas, coal provided only 34% of US electricity generation in 2015, down from 39% in 2014 and from 50% at its peak in 2005.

– Renewables continue to pick up steam, with an estimated 8.5GW of wind and 7.3GW of solar photovoltaic (PV) installed in 2015. Wind build was 65% above 2014 levels, as developers rushed to complete construction ahead of the anticipated end-2016 expiration date of the Production Tax Credit. In total, 2015’s tally of 16.4GW fell just shy of 2012’s record 18.2GW of new renewable capacity; however, PV additions across both the distributed and utility-scale sectors set new records as 2.9GW and 4.4GW, respectively, connected to the grid. This represents a 13% bump up from 2014 build for PV. New hydro build hit 306MW (+115% from 2014) and geothermal added 61MW of new capacity (+33%). Biomass, biogas and waste-to-energy together added 224MW, up 15% from the year before.

– As natural gas prices sank to their lowest levels since 1999 and natural gas plants displaced generation previously provided by retiring coal plants, natural gas consumption in the power sector exceeded 10quads for the first time ever, surpassing 2012’s high-water mark of 9.8quads. Natural gas is now within striking distance of being the largest source of US power, producing just over 32% of US generation in 2015, compared to 34% for coal.

– Importantly, surging renewables build and coal retirements have not triggered a dramatic leap in retail power prices. Average retail electricity rates across the country remain 5.8% below the recent peak (2008) in real terms, in part due to cheap generation from natural gas. Year on year, retail rates in 2015 fell 1.3% in real terms, even as real GDP grew by 2.4%. There are, however, regional price differences. New York, Texas, the Southeast and states in the central southern US reaped the greatest price reductions over the past year (over 2%) and generally have the lowest retail prices in the country. California saw the largest uptick (1.8%) and, alongside New York and New England, has some of the highest retail prices in the contiguous US.

– The continued low cost of power allows the US to potentially out-compete a number of other countries on electricity charges for businesses, with average industrial retail rates in the US (7.1¢/kWh in 2014) far below those of Germany (15.9¢/kWh), China (14.3¢/kWh) and even India (10.7¢/kWh).

– Corporate procurement of clean energy continues to grow, doubling from 2013 to 2014 and again from 2014 to 2015. In 2015 alone, corporations contracted 3.1GW of new renewable capacity. Although wind farms make up the majority of this contracted capacity, solar jumped from 0.3GW in 2014 to 1.1GW the following year, quadrupling its share of the overall pie. Large corporate buyers included Google, Amazon, Facebook and Apple; the list of key players covered the retail, technology, manufacturing, financial and insurance sectors. Additionally, corporations such as IKEA, Comcast, Hyatt, Morgan Stanley, and Johnson & Johnson announced and/or commissioned fuel cell capacity in 2015.

click to enlarge

click to enlarge• The evolution of US power is rapidly reducing the country's overall carbon footprint.

– The changes that have taken place over the past decade through 2015 resulted in the lowest yearly carbon emissions produced by the US power sector since 1995. At 1985Mt, the 2015 emissions figure was 4.3% below 2014 levels and 17.8% below 2005 levels. Two thousand five is both the benchmark against which the Clean Power Plan is measured, and against which the Obama administration set the goal of 26-28% emission reduction by 2025 contained in the US’ Intended Nationally Determined Contribution (INDC) for the UN climate talks in Paris.

click to enlarge

click to enlarge• Critical policy supports have been unveiled that, if fully implemented, will ensure the US remains on track to a lower-carbon energy sector.

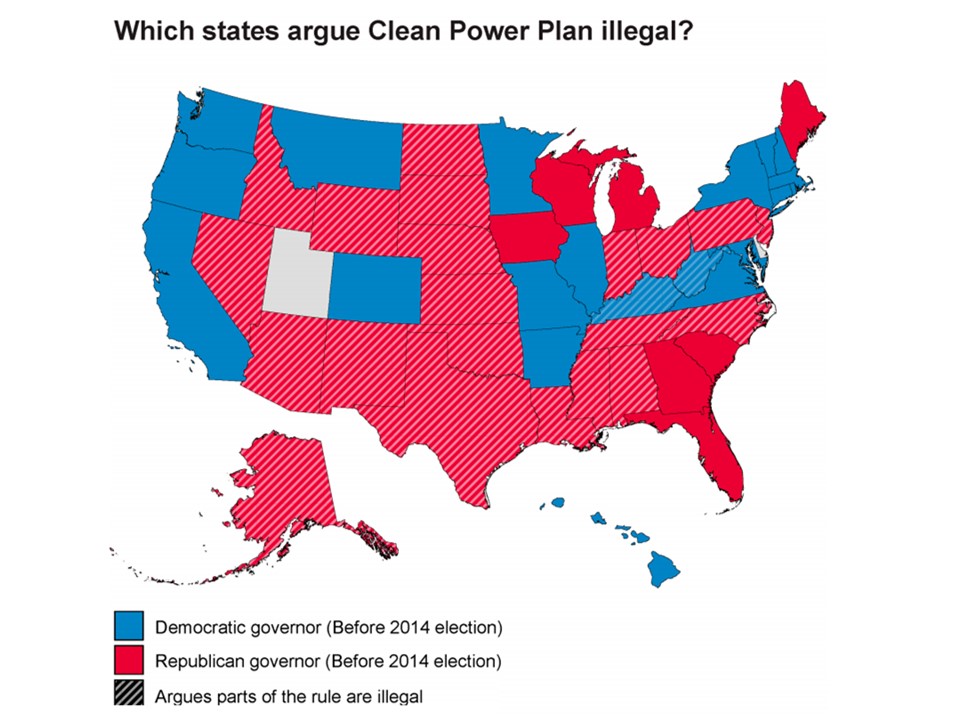

– The Obama administration sought to give policy certainty to the power industry and accelerate the de-carbonization of the US grid by finalizing regulations limiting carbon emissions from power plants in August 2015. The Clean Power Plan, which will regulate the country’s existing fleet of fossil-fired power plants, aims to cut emissions 32% (relative to 2005 levels) by 2030 through assigning each state a target emissions level (in tons of carbon) or emissions rate (in tons per megawatt hour). As the centerpiece of the Obama Administration’s INDC, the Plan was also supported by the New Source Performance Standards (NSPS) which set limits on emissions from newly constructed plants and will effectively require new coal-fired power plants to install carbon capture and storage technology.

– The Clean Power Plan’s reduction burdens (as measured by required cuts to emissions levels) vary widely across states. Those on the West Coast and in New England face smaller reduction targets that they are already on track to meet, while more coal-reliant states like Montana, the Dakotas and Kansas must cut emission levels by over 30%, even after accounting for recent and planned abatement actions such as coal retirements. To achieve these targets, states must design and carry out their own implementation programs, which will likely require a combination of coal-to-gas switching, renewables build and demand reduction measures such as energy efficiency. State proposals are due to the EPA by September 2018 and will be implemented from 2022 to 2030.

– In mid-December, 195 countries came together to sign the “Paris Agreement.” The Agreement is effectively a hodgepodge of bottom-up pledges from individual countries, including the US pledge to bring emissions to 26-28% below 2005 levels by 2025. Paris marks only one small milestone on the path to halting global climate change: as they stand today, the pledges would be insufficient for hitting the “below 2ºC” goal. But the agreement’s framework also includes five-year “check-ins” at which countries are encouraged to re-submit and strengthen their commitments.

– On December 18, Congress passed comprehensive spending and tax packages which revived critical federal supports for segments of the renewable energy and energy efficiency industries, while also lifting a 40-year-long ban on crude oil exports. The bill extended tax credits for wind and solar by five years apiece, through 2019 and 2021, respectively. Federal tax incentives for both technologies will be stepped down over the five-year periods. The Production Tax Credit for other renewable technologies (including biomass, geothermal, waste-to-energy and hydroelectricity) was only given an additional two years, through end-2016. The Investment Tax Credit for fuel cells was unchanged and will expire at the end of 2016. Energy efficiency incentives for residential, industrial and commercial investments were prolonged through December 31, 2016. Efforts are already underway to ensure these other clean energy technologies see their credits expanded further in 2016.

– Just after the close of the year, on January 25, 2016, the US Supreme Court issued a key ruling that would effectively allow ”demand response” (DR) programs to continue among large end-users. The Court upheld the Federal Energy Regulatory Committee’s authority to regulate DR within the wholesale energy markets. The decision brings several years of uncertainty to an end for DR players and should allow the market to flourish more broadly. Currently DR, which incentivizes industrial users to cut their consumption at times of excessively high demand, is most popular within the PJM Interconnection, a wholesale electricity market covering a number of mid-Atlantic and Northeastern states.

– In much of the country, state policy is as important as federal in advancing clean energy and the underlying infrastructure necessary to support it. For example, state and local “net energy metering” (NEM) policies and utility rate designs are essential to the economics of distributed generation. Two thousand fifteen saw two significant and differing regulatory proposals for addressing NEM. California unveiled a second-generation “NEM 2.0” program which maintains a net metering regime, with requirements that solar customers move to time-of-use rates, pay an upfront interconnection fee and pay the same nonbypassable charges as customers without a solar system. Neighboring Nevada adopted NEM program changes that alter the rates charged and credits granted to customers with rooftop solar, changing the economics for both existing and future solar customers. Similar proceedings regarding NEM and rate design policies are underway elsewhere, as states consider the implications of further growth in distributed generation and how to balance the need to advance deployment, while addressing concerns over potential rate inequities between solar-owning and non-solar-owning ratepayers, which could affect future investments in the underlying grid infrastructure.

click to enlarge

click to enlarge– Another form of critical state policy is the renewable portfolio standard (RPS) – a state mandate on the share of utility-delivered power provided by clean energy. RPS are the main driver behind wind and solar build in the Northeast; they incentivize renewables generation in other states as well. In 2015, Hawaii increased its target to 100% renewables by 2045, while California and New York raised their targets to 50% by 2030. Meanwhile, West Virginia became the first state to repeal its RPS and Kansas turned its mandatory standard into a voluntary program.

– Energy efficiency resource standards (EERS) have advanced in the past decade, but momentum slowed after 2010. Florida and Indiana removed their programs in 2014, Ohio froze its scheme in 2015 and federal support of energy efficiency did not receive the fiveyear extension that was granted to wind and solar investments. However, a handful of states including Delaware, Utah and New Hampshire are on their way toward adopting EERS. Additionally, the final Clean Power Plan has an option for states to count energy efficiency measures toward compliance.

– Nevertheless, state and local governments continue to enact other critical policies to promote energy savings, with 10 states adopting more stringent residential and commercial building codes in 2015, including Texas, California and New Jersey. Three cities, including Atlanta, enhanced building energy use policies, setting mandates for commercial buildings to report and benchmark their consumption. As of the end of 2015, 6.5bn square feet of commercial floor space, or around 7.7% of total US commercial sector floor space, was covered by such policies.

click to enlarge

click to enlarge• A ‘new normal’ of lower oil prices is being felt through the US economy and offers both opportunities and potential obstacles to the greening of US energy.

– Lower gasoline prices dented sales of alternatively-fueled vehicles in 2015. Hybrid and plug-in hybrid vehicles, which compete more directly with traditional gasoline-fueled cars, took the biggest hit: sales of these two vehicle classes were down 16% and 24%, respectively, relative to 2014. But other equally important factors were also at play, including supply constraints and delays in new model rollouts that dampened sales in the first half of 2015.

– However, sales of battery electric vehicles (BEV) proved resilient, growing 16% over the course of 2015, relative to 2014 levels. State and federal purchasing credits help to keep the lifetime costs of BEV ownership up to 25% below that of comparable midsize gasolinefueled cars. Additionally, a significant amount of BEV purchases – notably, those of the Tesla Model S – continue to be motivated by non-economic factors.

– Overall, gasoline consumption rose 4.1% in 2015, the largest annual increase since 1988, as prices at the pump fell an additional 11% after collapsing by one third in 2014. For the first time since record-keeping began in 2008, the average fuel economy of vehicles sold for model year 2015 stayed flat relative to the previous year, at 25.3mpg. In previous years, the impact of Americans’ preference for SUVs and pick-up trucks had been tempered by both higher oil prices and improving vehicle efficiency, in line with federal Corporate Average Fuel Economy (CAFE) standards Over the past year and a half, however, the collapse of retail gasoline prices by more than 40% was enough to stall the annual gains in vehicle efficiency. But 2015 may prove to be an anomaly: the average fuel economy of vehicles sold remains 20% above that of 2008 levels, and continued hikes in CAFE requirements should ensure a return to this trend over the long term.

click to enlarge

click to enlarge– Natural gas production and storage inventories reached all-time highs in 2015. Sustained low energy prices have prompted oil and gas producers to decrease drilling activity; hence, fewer rigs are in operation, leading to more competition amongst rig operators. Service companies have slashed fees in response, allowing drilling and completion costs to fall for oil and natural gas wells alike. In addition, improved technology and experience have enabled producers to continue to produce natural gas at even lower costs, with many of them focusing on regions with the most favorable production economics. Together, these factors have buoyed supplies in a depressed price environment. In December 2015, natural gas prices fell to the lowest levels seen since 1999.

– Thus, although lower-priced crude has little direct effect on the power sector (oil is burned for less than 2% of US generation), it has indirectly impacted the electricity markets by helping to weigh down natural gas prices. Natural gas-burning power plants substantially influence power prices across the US. As gas prices have fallen, so have wholesale power prices. For power generators bidding into the wholesale electricity markets, the decrease in power prices has squeezed profit margins. The lower-priced gas environment changes the equation for all power generators operating in deregulated markets, by potentially lowering future revenue streams.

– For technologies such as solar thermal and solar PV, falling power prices can make “grid parity” that much more difficult to achieve. However, generation costs associated with renewables have also been dropping. In windy parts of the country like Texas and the Midwest, wind developers have signed long-term power purchase agreements (PPAs) in the range of $19-35/MWh, undercutting both on-peak and off-peak power prices as well as other sources of generation. Also in Texas, utility-scale solar plants have achieved PPAs at rates close to $50/MWh, and in regions with either high retail electricity rates or high solar PV capacity factors, distributed solar can be an economically competitive option for homeowners. These falling costs, combined with the anticipated drawdown on the federal Investment Tax Credit and the expiration of the Production Tax Credit, led to significant build in solar and wind in 2015. New build in solar (7.3GW) and wind (8.5GW) outpaced even that of natural gas (6.0GW). Wind in particular marked a 65% increase in build from the previous year. Geothermal, hydro, biomass, biogas and waste-to-energy saw 0.6GW of build. New capacity additions in 2015 for geothermal jumped one-third from the previous year, while biomass, biogas and waste-to-energy saw a 15% bump. The rate of hydro installations soared 115% during the same period.

click to enlarge

click to enlarge• The US continues to extract unprecedented volumes of natural gas thanks to greater productivity from existing resources. This extraordinary resource is being put to use in a growing variety of ways.

– Low gas prices are further supported by Appalachian Basin shale production, which continues to expand despite a shrinking rig count as producers drill more selectively and technologies improve. Output from the Marcellus and Utica shales has been so abundant that domestic natural gas production through the first nine months of 2015 increased 6.8% from 2014 and 26% from 2007 levels, even as traditional "dry" gas production has declined.

– With the natural gas center of supply rapidly shifting from the Gulf Coast to the Northeast, midstream companies are playing catch-up to reverse existing pipelines and to re-plumb the network to transport gas out of the inundated Appalachian Basin. In 2015, companies installed over 11Bcfd of total pipeline capacity across the country, including 3.3Bcfd of takeaway capacity from the Marcellus and Utica shales. Many more projects were approved or filed for approval this year, but due to routine delays, the bulk of these projects are not expected to be in service until 2017 or 2018.

– Gas utility construction expenditures for distribution infrastructure rose to $9.7 billion in 2014, compared to an average of about $5 billion per year during the 2000s, according to data compiled by the American Gas Association. This reflects, in part, the increased prevalence of natural gas replacement and expansion programs across the US.

click to enlarge

click to enlarge• Investment in zero-carbon energy and enabling technologies maintains its momentum:

– Since 2007, the US has poured $445bn into renewable energy and energy smart technologies, which enable the integration of variable sources of power generation into the grid. Annual totals range from $36bn to $64bn; investment in 2015 hit $56bn, up 8% from the year before. Just over half of all new investment was directed towards solar, and 21% towards wind. The increase came as project developers rushed to get projects online ahead of the anticipated expiration of critical federal tax credits, and as falling costs made rooftop solar economically competitive in parts of the country.

– Asset financing, which includes only investment in new projects, for biomass facilities rebounded to $349m in 2015 from none the previous year; biogas received $285m in 2015, about seven times what it saw in 2014. The rush was again due to tax credit considerations. At the same time, flows into other renewables continue to taper, with virtually no new financing directed towards new construction in geothermal, small hydro or carbon capture and storage in 2015. Waste-to-energy has not seen asset financing since 2012. Outside of the power sector, energy smart technologies attracted $3.1bn, with Tesla Motors leading the pack.

– Investment in key infrastructure to support the transformation of the grid remains critical and continues to lag the rapid build-out of renewable technologies in some regions of the country. Transmission constraints in high wind-build areas such as the Midwest, for example, have led to the curtailment of generation from zero-carbon sources. In 2014, investor-owned utilities invested $98bn in upgrading the electric grid; early estimates put forward by the Edison Electric Institute suggest $20bn was directed towards transmission. In Texas, a multi-year $7bn investment in the Competitive Renewable Energy Zone (CREZ) has allowed the state to connect up to 18GW of wind capacity in the West and the Panhandle to load centers in the Southeast, helping to relieve transmission congestion costs and reduce curtailment. Several large projects, currently in the planning stage, hope to follow Texas’ lead by building new lines connecting wind in Kansas and Iowa to demand in the Midwest and Mid-Atlantic.

– Globally, the US held its place as the second-most attractive country for clean energy investment – but it remains far behind China, which received $111bn worth of capital flows into the sector compared to the US’ $56bn. Other APAC countries brought in $58bn, while investment in Europe fell off dramatically to $59bn from $72bn in 2014. • Renewable energy technologies are a substantial and growing portion of the overall US power matrix. – Renewables including large hydro now make up 20% of the US plant stack, at 222GW. Hydroelectric facilities and pumped storage represent nearly half of this at 102GW – a figure that has stayed roughly constant since 2008. Wind is the second-most prevalent renewable technology, standing at almost 75GW at the end of 2015, roughly triple its installed capacity at the end of 2008 (25GW). But solar has been the fastest growing, averaging a 60% clip annually since 2008 to bring its total capacity to 28GW.

click to enlarge

click to enlarge– Geothermal, biomass, biogas, and waste-to-energy additions have grown at a slower pace, with 3.2GW added collectively since 2008. Capacity for biomass, biogas and wasteto-energy reached a total of 13.5GW in 2015, 15% above 2008. Geothermal installations have also risen 15% since 2008, to finish 2015 at 3.6GW. These technologies provide around-the-clock power at levelized costs comparable to those of other renewables, but they have not enjoyed the same policy support as the wind and solar industries. They continue to represent roughly 17GW of capacity across the country. Hydropower, for its part, is also supported differently compared to wind and solar, which has meant that installed capacity has stagnated at just under 102GW since 2008.

– Distributed generation, driven by solar PV, is playing a rapidly growing role in the renewable energy story. 2015 was yet another record year for distributed solar PV in the US, with 2.9GW of new build due to growth in both the commercial and residential sectors. As a result, cumulative distributed PV capacity in the US now exceeds 11GW. Build for combined heat and power (CHP) installations ticked up 25% over 2013 levels, clocking in at 847MW in 2014, due to greater demand from the industrial sector. Cheaper gas has also incentivized CHP generation, which soared from 304TWh in 2013 to over 360TWh in 2014 and 2015. However, not all news is good for distributed generation outside of solar. Growth in CHP is still hampered by the lack of supportive federal or state policies. Activity in other distributed, smaller scale technologies has also been muted, with only 6MW of small- and medium-scale wind built in 2014 and three small-scale biogas projects in 2015.

– Behind-the-meter storage has grown in popularity among commercial and industrial players in states such as California, Hawaii and New York, where utilities set high demand charges. Some of the storage projects are supported by subsidies such as the SelfGeneration Incentive Program (SGIP) in California, which offers $1.46/W for a storage system and has induced the installation of 119 projects, or 2.4MW of commercial storage in the state. The economics for residential distributed storage have been less favorable as net metering and lack of time-of-use tariffs limit its economic case. However, utilities such as Southern California Edison, Con Edison, and the Hawaiian Electric Company have begun to explore aggregated distributed storage (sometimes with solar). Companies including Sunverge, Stem, Green Charge Networks and Advanced Microgrid Systems have started piloting advanced storage management systems to coordinate and aggregate distributed storage (sometimes also coupled with solar or other generation sources). In 2015, aggregated storage bid successfully into California's real-time power market; the technology can also provide grid services.

2015 was a transformative year in the US energy industry. Greater energy efficiency and structural changes to the composition of the economy allowed the US to achieve higher energy productivity. The power sector continued to de-carbonize and add near-record amounts of clean energy as policy activity at the global, national and state levels set the country on track for further emissions abatement. Unprecedented levels of natural gas supply pushed down power prices, putting the country in a more internationally competitive position while also prompting coal-to-gas switching that slashed US carbon emissions. Utilities are investing more in energy efficiency measures to curb both electricity and gas demand. At the same time, the grid itself is being reshaped by greater penetration of renewables and growth in distributed resources such as solar PV and storage. The policy frameworks laid out in 2015, combined with the beginnings of structural change in the power sector and beyond, are pushing the country toward greater energy productivity and cleaner growth in the decades to come.

posted by Herman K. Trabish @ 9:09 AM

0 comments

![]()

click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge click to enlarge

click to enlarge

Plug-in Hybrids, The Cars That Will Recharge America

Plug-in Hybrids, The Cars That Will Recharge America Oil On The Brain

Oil On The Brain